Key Takeaways — What You’ll Learn in This Guide

- What a hard money loan is and exactly how it works — from application to balloon payment.

- Current 2025 interest rates: national average ranges from 8% to 14%, with most borrowers landing between 9.5% and 12%.

- The 5 qualification factors lenders actually scrutinise — and which ones matter most.

- How hard money compares to conventional loans, bridge loans, and private money — side by side.

- A real case study showing how leveraging hard money turned $600K cash into $315K profit — vs. $90K without it.

- When you should walk away from a hard money loan and choose something else entirely.

Imagine spotting a distressed property at a price that makes your numbers sing — but a bank’s 45-day approval process means you’ll lose it to a cash buyer tomorrow morning. That’s the exact problem that answers the question most investors type into Google at 11 PM: what is a hard money loan, and can it close this deal before the weekend?

The short answer: yes, often within 5 to 10 business days. The honest answer: at a price you need to understand completely before you sign anything.

This guide covers what is a hard money loan from every angle that matters — the mechanics, the real cost, the qualification criteria, the tax considerations, the alternatives, and a real-world case study showing what happens when investors use leverage correctly. We also cover what can go wrong, because this type of financing carries genuine risk when you’re not prepared for it.

What is a Hard Money Loan? The Definition That Actually Explains It

A hard money loan is a short-term, asset-based loan secured by real property and issued by a private lender — not a bank or credit union. The lender’s primary concern isn’t your credit score or your W-2. Their primary concern is the value of the property you’re using as collateral.

The name comes from the collateral itself. In lending circles, “hard” refers to a tangible, physical asset — in this case, real estate — as opposed to “soft” financing, which relies on your financial profile. A hard money loan is literally a loan backed by a hard asset.

The definition in practice: you find a property worth $300,000. A hard money lender agrees to fund up to 70–80% of its value — or in many cases, up to 70% of its After-Repair Value (ARV) if you plan to renovate. You receive the funds in days, not months. You renovate or reposition the asset, then sell or refinance to pay off the loan.

What Is a Hard Money Loan? Core Characteristics

- Interest-only structure: Most hard money loans require monthly interest-only payments, with the full principal balance due as a balloon payment at the end of the loan term.

- Short-term: Most hard money loans run from 6 months to 3 years and are not designed for permanent financing.

- Asset-backed: These loans are secured by real estate, meaning the property’s value drives the lending decision.

- Private lender: Hard money loans are issued by individuals, investment groups, or private lending companies rather than traditional banks or credit unions.

- Faster approval: Most hard money lenders can close deals within 5–14 business days, compared to 30–45+ days for conventional mortgages.

- Higher cost: Interest rates typically range from 8% to 15%, with origination fees between 1.5% and 3%. The speed and flexibility come at a higher cost.

“Hard money loans are the private equity of real estate finance — expensive capital deployed at speed for projects where timing creates value.”

— Keith Thomas, CEO of Private Capital Investors

Source: Private Capital Investors — 30+ years real estate and finance experience (privatecapitalinvestors.com)

The real estate market’s most competitive deals often don’t wait for underwriters. Foreclosures, auction properties, deeply discounted distressed assets — these situations reward whoever closes first. That’s what makes understanding what is a hard money loan so critical for serious investors.

The Real Cost: Hard Money Loan Rates, Fees, and What You Pay

Here’s where most guides stop at a vague range and leave you. We’re going deeper.

2025 Interest Rate Landscape

In 2025, national average hard money loan interest rates range from 8% to 14% annually, with most borrowers landing between 9.5% and 12% depending on lender competition, loan type, and property location — according to SDC Finance’s current lending data. California lenders typically quote 9%–13% due to higher property values and intense lender competition.

8%–14% National average range for hard money loan interest rates in 2025, with the majority of deals priced at 9.5%–12%.

Source: SDC Finance / SDC Capital, Hard Money Loan Rates 2025 (sdcfinance.com)

Rocket Mortgage’s own data puts conventional 30-year fixed rates at 6.26% as of September 2025. That means the hard money premium runs 2–8 percentage points higher. On a $300,000 loan, that’s a real number — and it’s the cost of speed, flexibility, and access.

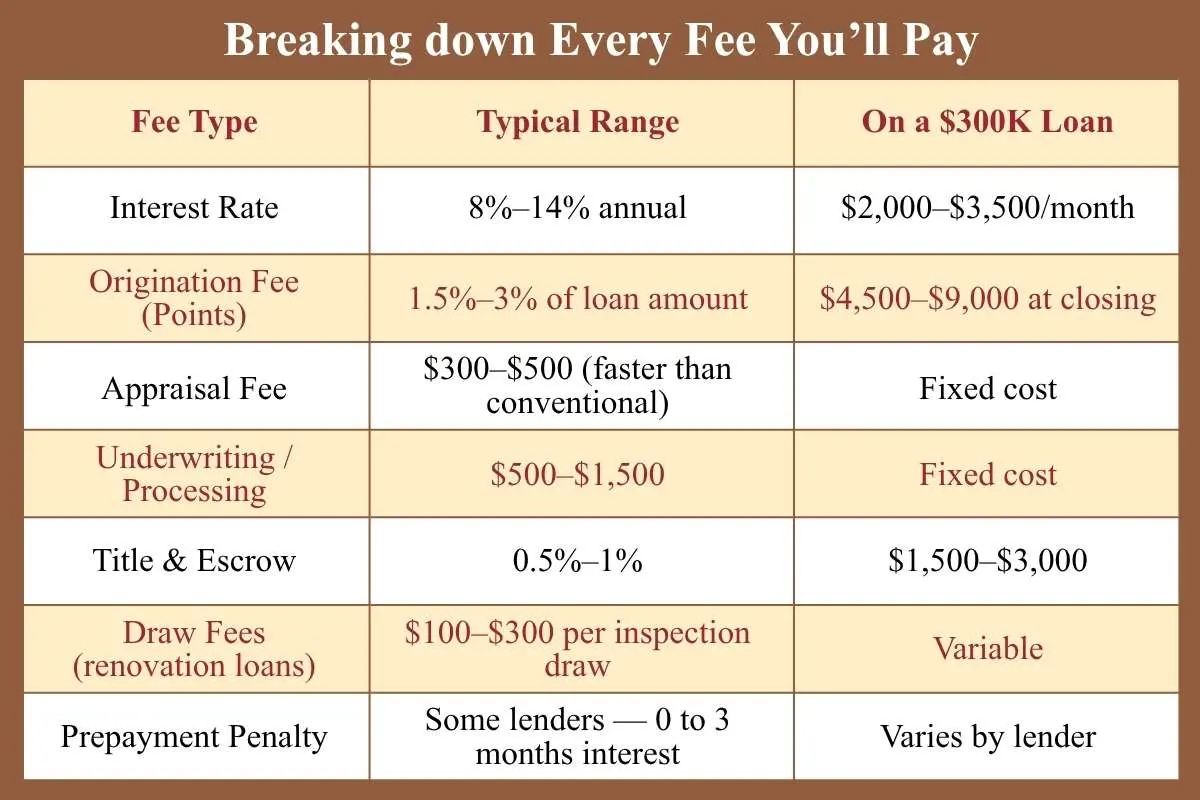

Breaking down Every Fee You’ll Pay

| Fee Type | Typical Range | On a $300K Loan |

| Interest Rate | 8%–14% annual | $2,000–$3,500/month |

| Origination Fee (Points) | 1.5%–3% of loan amount | $4,500–$9,000 at closing |

| Appraisal Fee | $300–$500 (faster than conventional) | Fixed cost |

| Underwriting / Processing | $500–$1,500 | Fixed cost |

| Title & Escrow | 0.5%–1% | $1,500–$3,000 |

| Draw Fees (renovation loans) | $100–$300 per inspection draw | Variable |

| Prepayment Penalty | Some lenders — 0 to 3 months interest | Varies by lender |

Macoy Capital’s data confirms origination fees land between 1.5% and 3%, with additional closing costs on top. If you borrow $300,000 and the lender charges 2.5 points plus 1% closing costs, you’re paying $10,500 in upfront fees before interest even starts accruing. That’s not a hidden cost — it’s a known cost. The discipline is building it into your deal analysis before you commit.

The Loan-to-Value (LTV) Reality

Most hard money lenders finance 65–80% of the property’s current (as-is) value, or up to 70% of the After-Repair Value (ARV) for fix-and-flip projects. LendingTree’s research confirms the typical range as 60–75% LTV.

Here’s what that means with numbers: if a property’s ARV after renovation is $500,000, a lender at 70% ARV caps the loan at $350,000 total. That covers purchase price plus renovation costs. Every dollar above that comes from your own pocket — by design.

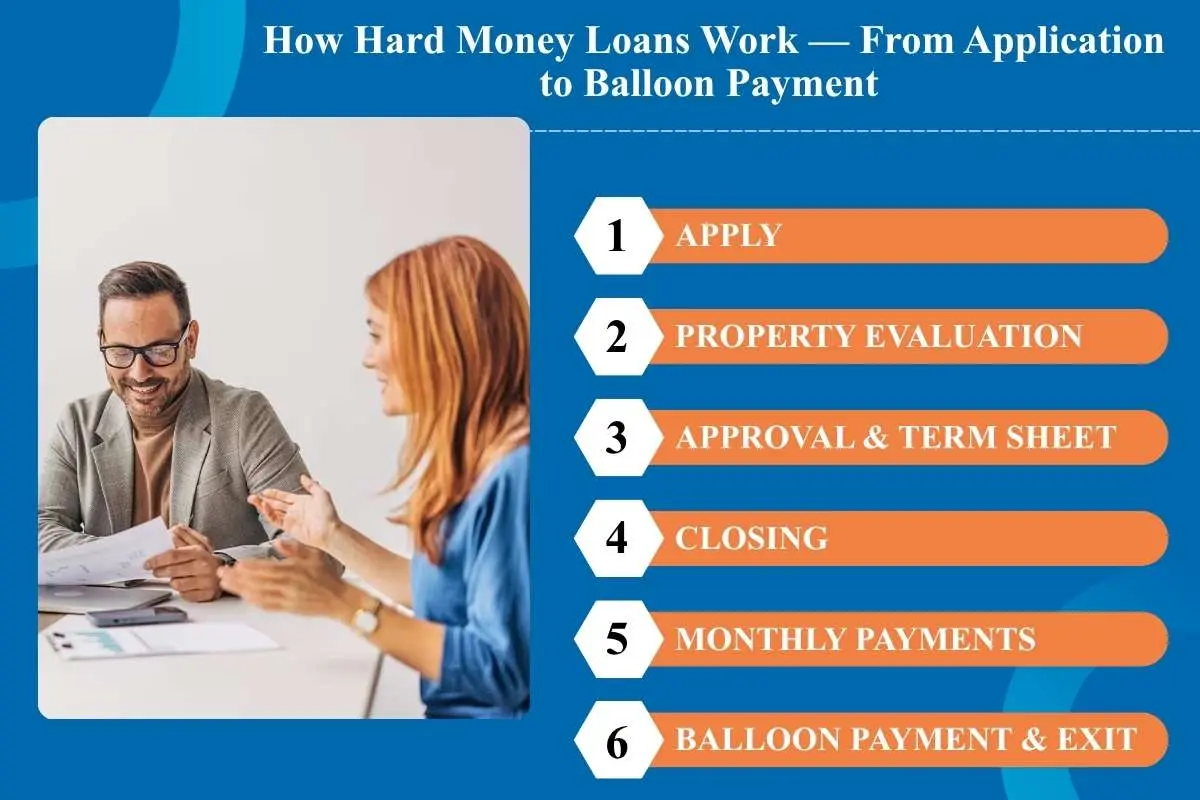

How Hard Money Loans Work: From Application to Balloon Payment

- Apply: Submit a brief loan summary — property address, purchase price, renovation scope, and your exit strategy. No lengthy income verification. No tax return review. Most lenders want a one-page deal summary and a recent bank statement to confirm reserves.

- Property Evaluation: The lender orders an appraisal or Broker’s Price Opinion (BPO). They evaluate as-is value and, for renovation projects, the ARV. This typically takes 3–5 business days.

- Approval & Term Sheet: The lender issues a term sheet with rate, points, LTV, and repayment structure. Review this carefully. Compare it against at least two other lenders before signing.

- Closing: Once you accept the terms and clear title review, the loan closes. Hard money loans routinely close in 5–14 business days — versus 30–45+ days for a bank loan.

- Monthly Payments: Most hard money loans use an interest-only structure. On a $300,000 loan at 12%, your monthly payment is $3,000 — none of it principal. The principal waits.

- Balloon Payment & Exit: At the end of the term (typically 12–18 months for fix-and-flip), you repay the full principal balance — the balloon payment — either through property sale proceeds or refinancing into a conventional loan.

Important: The Balloon Payment Risk

Hard money lenders rarely grant extensions if you can’t repay on schedule. If your renovation runs long, the property won’t sell, or you can’t refinance in time, you face default — and the lender can foreclose on the collateral property. Build extra time into every timeline. The most experienced investors pad their exit strategy by 30–60 days.

Who Uses Hard Money Loans and the Specific Situations Where They Win?

House Flippers and Fix-and-Flip Investors

This is the dominant use case. In Q3 2024 alone, 74,618 single-family homes and condos were flipped, representing 7.2% of all sales that quarter, per RCN Capital data. The average gross profit on a flip in 2025 sits at $73,500, with a 30.4% average ROI. But those numbers only work for investors who understand what is a hard money loan and close fast enough to get the deal.

Hard money loans fund quickly enough to compete with cash buyers at auction and in off-market transactions. A traditional mortgage would arrive too late.

$73,500 Average gross profit per house flip in 2025, with a 30.4% average ROI. 88% of flips succeed, per 2025 industry data.

Source: RCN Capital, 2025 Hard Money Loans: Why Brokers Need Them Now (rcncapital.com)

Real Estate Investors Who Don’t Qualify for Conventional Financing

Investors with non-standard income — self-employed, multiple LLCs, recent foreclosure, or high DTI ratios — often can’t satisfy a bank’s documentation requirements on short timelines. Hard money lenders don’t rely on your W-2. They rely on the property’s value and your exit plan.

According to Rocket Mortgage, some borrowers with a spotty credit history or a history of delinquencies may face higher rates but can still qualify for hard money where conventional channels are closed.

Commercial Property Buyers

Business owners acquiring commercial real estate, especially properties needing significant renovation or properties that don’t meet standard bank requirements, use hard money as a bridge to long-term conventional financing. The strategy: acquire and stabilise the asset using hard money, then refinance into a commercial mortgage once the property is income-producing and appraised at its improved value.

The BRRRR Strategy (Buy, Rehab, Rent, Refinance, Repeat)

The BRRRR method specifically pairs hard money with long-term rental financing. Step 1: buy and rehab with hard money. Step 2: place tenants. Step 3: refinance into a DSCR loan or conventional rental mortgage at the improved appraised value. Step 4: pull out your equity, repay the hard money loan, and redeploy into the next deal. This cycle is how professional real estate portfolios scale.

What Hard Money Lenders Actually Look At: The 5 Qualification Factors

Unlike conventional mortgage underwriting — which runs your income, employment history, credit score, and debt-to-income ratio through a 45-day process — hard money qualification centres on five specific factors. Constitution Lending and Macoy Capital, both active private lenders, document these clearly in their underwriting guidelines for borrowers researching what is a hard money loan.

| Qualification Factor | What It Means | Why It Matters |

| 1. Loan-to-Value (LTV) and ARV | Lend up to 70–85% of as-is value, or up to 70% of After-Repair Value | Protects lender in case of default — the property must cover the loan |

| 2. Exit Strategy | Clear plan to repay: property sale (flip) or refinance (BRRRR) | Lenders who don’t see a viable exit will decline regardless of other factors |

| 3. Credit Score | Minimum ~550–660 (varies by lender); less critical than in conventional loans | Signals willingness to pay; low credit = higher rate, not automatic denial |

| 4. Cash Reserves & Liquidity | 3+ months of loan payments in liquid reserves; down payment of 20–40% | Lenders want skin in the game; shows you can handle project overruns |

| 5. Project Experience & Scope of Work | Experienced investors get better terms; first-timers still qualify with strong plans | A detailed renovation budget from a licensed contractor builds lender confidence |

Constitution Lending sets a minimum credit score of 660, requires 3 months of loan payments in cash reserves, and lends up to 70% of ARV on fix-and-flip projects. But these aren’t universal — Macoy Capital takes a more holistic view, reviewing all relevant factors and specifically noting that a foreclosure in your past won’t automatically disqualify you.

“The biggest reasons hard money lenders walk away are gaps in equity, credit, experience, documentation, property condition, exit plan, and cash reserves. Identify which gap applies to your deal and address it before you submit.”

The Credit People Research Team

Source: TheCreditPeople.com, Hard Money Loan Requirements, April 2026 (thecreditpeople.com)

The Down Payment Reality

Hard money lenders almost always require a meaningful down payment. The typical range runs from 20% to 40% of the purchase price. This isn’t primarily about the lender’s risk management — it’s about ensuring you have skin in the game. An investor with 30% equity in a project has a strong incentive to complete it. An investor with 5% equity might walk away the moment a problem emerges.

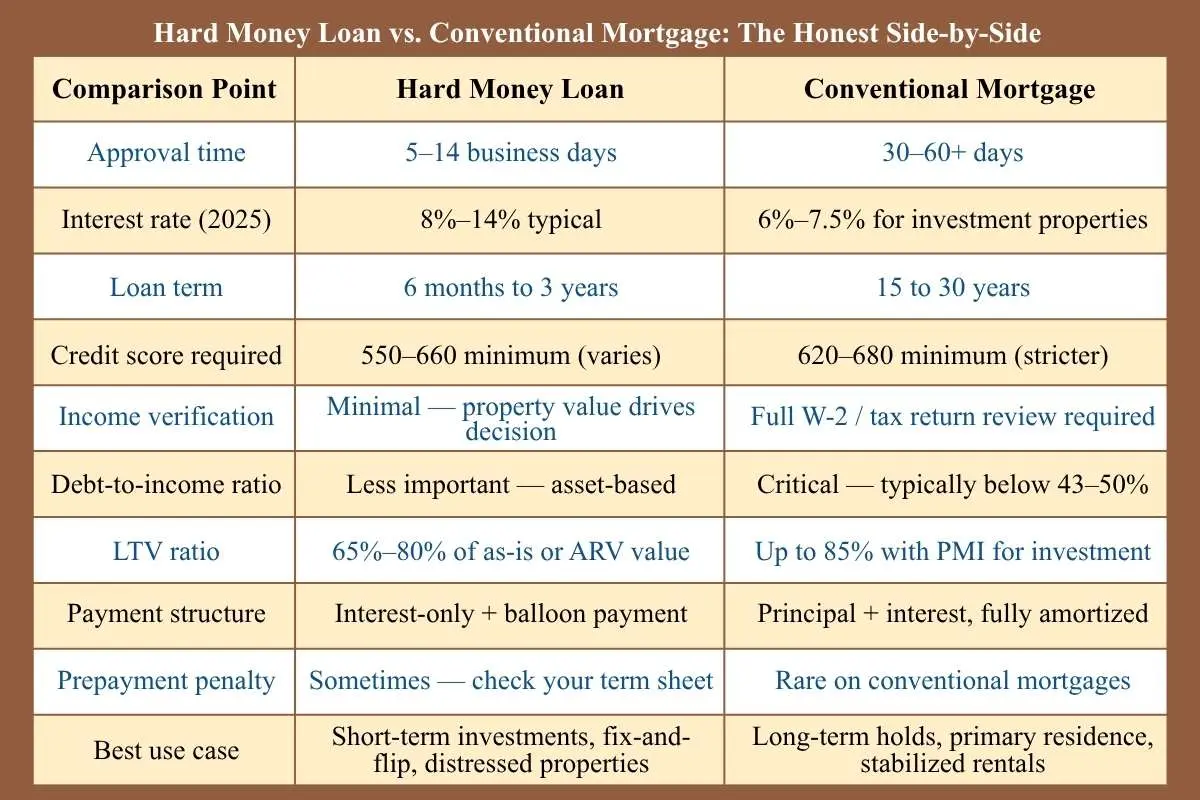

Hard Money Loan vs. Conventional Mortgage: The Honest Side-by-Side

The question isn’t which option is ‘better’ — it’s which one matches your specific situation. Here’s what each looks like in direct comparison.

| Comparison Point | Hard Money Loan | Conventional Mortgage |

| Approval time | 5–14 business days | 30–60+ days |

| Interest rate (2025) | 8%–14% typical | 6%–7.5% for investment properties |

| Loan term | 6 months to 3 years | 15 to 30 years |

| Credit score required | 550–660 minimum (varies) | 620–680 minimum (stricter) |

| Income verification | Minimal — property value drives decision | Full W-2 / tax return review required |

| Debt-to-income ratio | Less important — asset-based | Critical — typically below 43–50% |

| LTV ratio | 65%–80% of as-is or ARV value | Up to 85% with PMI for investment |

| Payment structure | Interest-only + balloon payment | Principal + interest, fully amortized |

| Prepayment penalty | Sometimes — check your term sheet | Rare on conventional mortgages |

| Best use case | Short-term investments, fix-and-flip, distressed properties | Long-term holds, primary residence, stabilized rentals |

The 30-year conventional mortgage rate averaged 6.26% in September 2025 (Rocket Mortgage data). At that rate, your monthly payment on a $300,000 loan is approximately $1,854 — fully amortized. At 12% hard money on a $300,000 interest-only loan, you pay $3,000 per month with nothing applied to principal. The hard money loan costs $1,146 more per month — but it closes in 7 days instead of 45, accepts a distressed property as collateral, and doesn’t require two years of tax returns, which explains what is a hard money loan in practical terms.

For the right deal with the right exit strategy, that premium is a sound business decision. For long-term rental financing, it’s a financial mistake.

Hard Money vs. Bridge Loan vs. Private Money — What’s the Actual Difference?

These three terms often get used interchangeably. They’re not the same, and the distinctions matter when you’re choosing between them.

Hard Money Loans

Short-term, asset-based, 10%–15%+ rates typical. Funded by private lenders, usually as companies. Focus: distressed properties, fix-and-flip, investors who don’t qualify for conventional financing. Higher rates reflect higher risk properties and borrowers.

Bridge Loans

Also short-term and private, but typically used for less risky scenarios, like bridging the gap between buying a new property and selling an existing one, or between acquiring a stabilised property and securing permanent financing. Because the risk profile is lower, bridge loan rates are typically 6%–10%, meaningfully cheaper than hard money rates. The mortgagecalculator.org confirms this distinction clearly.

Private Money Loans

Private money is the broadest term — any loan from a private individual rather than an institution. Hard money is a specific type of private money, but not all private money is hard money. A loan from a family member, a business partner, or a real estate syndicate is private money. Terms vary entirely by negotiation — sometimes rates below 6%, sometimes flexible repayment, sometimes equity-based.

| Loan Type | Rate Range | Best For | Risk Level |

| Hard Money | 10%–15%+ | Distressed properties, fix-and-flip, credit-challenged borrowers | Higher |

| Bridge Loan | 6%–10% | Stabilised properties, buying before selling, clear refinance path | Moderate |

| Private Money | Negotiated (2%–12%+) | Personal network, flexible terms, relationship-based deals | Variable |

| Conventional Mortgage | 6%–7.5% (investment 2025) | Long-term holds, stabilised income properties | Lower |

Case Study: How the Same $600K Produced 3.5x More Profit with Hard Money

This case study, documented by Anchor Loans, illustrates exactly why experienced investors use leverage even when they have cash available. The numbers tell the whole story.

Case Study — John & Jane Doe Company

Year 1: Cash Only (No Leverage)

- Available capital: $600,000 in cash reserves

- Properties purchased: 2 homes (entire capital deployed)

- Net profit per flip: $45,000

- Total net profit: $90,000

- ROI: 15%

Year 2: Hard Money Leverage

- Available capital: The same $600,000 used as down payments

- Properties purchased: 9 homes (hard money funded the majority)

- Average profit per flip after hard money costs: $35,000

- Total net profit: $315,000

- ROI: 52%

The interest and fees on the hard money loans reduced the per-deal profit from $45,000 to $35,000. But accessing nine deals instead of two multiplied the total return by 3.5x. This is the core case for hard money leverage in fix-and-flip investing: the cost of borrowed capital is a small price relative to the deals you would have missed.

$72,000 Average profit per house flip in 2024 nationwide — but only for investors who could fund quickly, per ATTOM Data Solutions research.

Source: OfferMarket, Real Estate Hard Money Loans for Flipping Houses (offermarket.us), citing ATTOM Data Solutions 2024.

“In the house flipping business it is often said that ‘cash is king’ — but leverage done right turns a single dollar into four.”

Anchor Loans Editorial Team

Source: AnchorLoans.com, ‘Using Hard Money Loans for House Flipping: The Pros and Cons’ (anchorloans.com).

The Risks of Hard Money Loans: What Can Go Wrong

Every tool has failure modes. A hard money loan is powerful in the right situation and genuinely dangerous in the wrong one. Here are the specific risks, sourced from lender and investor experience.

Risk 1: The Project Runs Over Time

Hard money loans at 12% cost $1,000 in interest per month per $100,000 borrowed. Six months of holding costs on a modest project, including interest, taxes, insurance, and utilities — can easily exceed $10,000. If your renovation takes four months instead of two, those extra months eliminate a significant portion of your projected margin.

Risk 2: The Market Shifts Mid-Project

The Q2 2025 gross flip ROI of 25.1% sounds solid until you apply costs. Flipping veterans estimate operating expenses consume 20%–33% of ARV. On a $325,000 sale, that’s $65,000–$107,000 in costs. When your gross profit is only $65,300, you’re operating at paper-thin margins. A buyer demand dip or rate spike can erase those margins entirely.

Risk 3: You Can’t Refinance on Schedule

If the renovation isn’t complete when your loan expires, many hard money lenders won’t grant an extension. If you can’t sell or refinance in time, you face default and foreclosure on your collateral. Build exit strategy flexibility into every deal: plan to sell AND have a secondary plan to rent and refinance.

Risk 4: Predatory Lenders

Hard money lenders operate under less regulatory oversight than banks. Some lenders impose hidden fees, arbitrary default triggers, or interest rate changes. The Wolters Kluwer analysis confirms that hard money lending regulation varies significantly by state and many borrowers incorrectly assume these loans are exempt from federal protections like TILA and RESPA.

How to Protect Yourself: Verified Risk Management Steps

- Always compare at least 3 lenders before committing. Rate and fee structures vary dramatically.

- Read the prepayment penalty clause. Some lenders charge 3 months of interest if you pay early.

- Verify the lender’s licensing in your state. Some states require mortgage broker’s licenses for hard money lending.

- Build a 60-day buffer into your project timeline. Expect delays. They happen on almost every renovation.

- Always have a secondary exit strategy — if you can’t sell, can you rent and refinance?Consult a real estate attorney before closing any hard money deal, especially for first-time borrowers.

Alternatives to Hard Money Loans — When Another Option Makes More Sense

Understanding what is a hard money loan is only useful if you also know when NOT to use one. Here are the primary alternatives and the situations where they outperform hard money.

| Alternative | Best For | Key Advantage Over Hard Money |

| Conventional mortgage | Stabilised rental properties, long-term holds with strong credit | 6%–7.5% vs. 8%–14% — far cheaper for holds over 2+ years |

| FHA loan | Owner-occupied multi-unit (live in one, rent others) | Low down payment, lower rate — but can’t use for pure investment |

| Home equity loan / HELOC | Existing homeowners with equity — funding next investment | Often 7%–9% vs. 12%+ — tied to your primary residence |

| Cash-out refinance | Investors with substantial equity in existing properties | Lower rate than hard money, longer term, no balloon payment |

| Bridge loan | Buying before selling existing property, stabilised collateral | 6%–10% — moderate cost, faster than conventional |

| Private money / partnership | Personal network, family investors, equity partnerships | Negotiated terms — sometimes cheapest capital available |

| Seller financing | Motivated sellers willing to carry a note | No bank required, flexible terms, sometimes below-market rates |

LendingTree’s hard money analysis recommends evaluating home equity loans, cash-out refinancing, and peer-to-peer lending as meaningful alternatives depending on your situation. For investors with strong credit and a clear 30-year hold, the conventional route costs significantly less in total interest paid.

How to Find and Vet a Hard Money Lender?

The hard money lender market has no shortage of participants but quality varies dramatically. An established private lender with clear guidelines and transparent fees is a very different business partner than a fly-by-night operation with buried clauses, which is why understanding what is a hard money loan matters before signing any agreement.

Where to Find Reputable Hard Money Lenders?

- BiggerPockets forum; the most active real estate investor community in the US, with detailed lender reviews and direct referrals from investors who have closed deals

- Real estate investment clubs and REIA (Real Estate Investor Association) meetings in your market

- Referrals from title companies, real estate attorneys, and experienced local flippers

- Direct search for licensed lenders in your state — verify their license through your state’s Department of Financial Institutions

The 8 Questions to Ask Before You Commit

- ‘What is your maximum loan-to-value ratio — on as-is value and on ARV?’

- ‘What are your typical loan terms — 6 months, 12 months, 24 months?’

- ‘Do you charge interest-only or principal and interest payments monthly?’

- ‘What origination fees, processing fees, and closing costs apply to this specific loan?’

- ‘Do you charge a prepayment penalty if I pay off the loan early?’

- ‘How do you handle extension requests if the project runs over time?’

- ‘Are you licensed in my state, and under what regulatory framework do you operate?’

- ‘Can you provide references from borrowers who have closed similar deals with you?’

“Behind every great company are the people who provide the service. A hard money lender should feel like they’re just as invested in your success as you are — because if your deal works, they get paid.”

Robert W., Broker Partner (verified Trustpilot-equivalent review)

Source: Easy Street Capital client review, April 2024 (easystreetcap.com)

Frequently Asked Questions about Hard Money Loans

1. What is a hard money loan in simple terms?

A hard money loan is a short-term loan backed by real estate, issued by a private lender rather than a bank. The lender cares primarily about the property’s value — not your credit score or income. These loans close fast (5–14 days), carry higher interest rates (8%–14%), and typically last 6 months to 3 years. They’re designed for investors who need speed and flexibility that conventional banks can’t offer.

2. What are the typical interest rates on hard money loans?

In 2025, national average hard money loan rates range from 8% to 14% annually. Most borrowers in competitive markets land between 9.5% and 12%. Conventional 30-year mortgages averaged 6.26% in September 2025 (Rocket Mortgage data), making hard money 2–8 percentage points more expensive. The premium pays for speed, flexibility, and access to deals that conventional financing can’t touch.

3. What credit score do you need for a hard money loan?

Most hard money lenders accept credit scores in the 550–660 range or higher, though requirements vary significantly by lender. Some lenders set a minimum of 500. The key distinction: a low credit score won’t automatically disqualify you the way it would for a conventional loan — lenders are far more focused on the property’s value and your exit strategy than your credit history.

4. How do you repay a hard money loan?

Most hard money loans use an interest-only payment structure throughout the loan term, followed by a balloon payment of the full principal balance at maturity. Common exit strategies include: selling the renovated property (fix-and-flip), refinancing into a conventional or DSCR rental loan (BRRRR strategy), or using proceeds from another asset sale. Lenders rarely grant extensions — build your timeline with buffer.

5. What is the difference between a hard money loan and a private money loan?

Hard money is a specific type of private money. Both come from non-bank, private lenders. The distinction: hard money typically refers to company-based private lenders with set guidelines, higher rates (10%–15%+), and a focus on distressed real estate. Private money is broader — it can include loans from individuals, family, friends, or partners at negotiated terms, sometimes far below market rates.

6. Can you use a hard money loan to buy a primary residence?

In practice, hard money loans almost exclusively target investment and commercial properties. Most hard money lenders explicitly state they do not lend on owner-occupied properties. Even lenders who technically could lend on primary residences face heavier regulatory scrutiny under TILA and state consumer protection laws for owner-occupied loans. For a primary residence, conventional, FHA, or VA loans are the appropriate path.

7. What is the 70% rule in hard money lending?

The 70% rule states that an investor should pay no more than 70% of a property’s After-Repair Value (ARV), minus estimated repair costs. This is both an investor guideline and a hard money lender benchmark: most lenders set their maximum loan at 70% of ARV to protect against default. Example: ARV $400,000 × 70% = $280,000 maximum loan. Subtract $60,000 in repairs = maximum purchase price of $220,000. This rule is central to understanding what is a hard money loan and how lenders manage risk.

8. How fast can you close a hard money loan?

Most established hard money lenders close loans in 5–14 business days. Some specialised lenders advertise closings in 24–48 hours for experienced borrowers with clean deals, though these typically require a pre-established lending relationship. Compare this to conventional mortgages at 30–60 days. The speed difference is the primary reason investors pay the hard money premium on time-sensitive opportunities.

Sources & Citations

- Rocket Mortgage — ‘What Is a Hard Money Loan?‘.

- Macoy Capital — ‘Hard Money Loan Rates 2024’.

- LendingTree — ‘What Is a Hard Money Loan? Lenders, Requirements and Rates’.

- Constitution Lending — ‘Hard Money Loan Requirements’.

- Wolters Kluwer — ‘Do Hard Money Lenders Need to Be Licensed?’.

- MortgageCalculator.org — ‘Hard Money Loan Calculator & Rates Comparison’.