You sit at your kitchen table, looking over your home loan statement. The monthly payment feels heavier than it used to, and you remember locking in your rate years ago when things were different. Now, with changing interest rates and shifting financial goals, you start wondering if your mortgage could work better for you.

Many homeowners reach this point after a few years. It often leads to exploring ways to adjust their loan without giving up the home they worked hard for. But

But How does refinancing work when it comes to a mortgage? Understanding that can help you see how replacing your current mortgage with a new one might lower your payments, reduce your interest rate, or give you more control over your finances.

What do you mean by refinancing a mortgage?

Refinancing a mortgage means you replace your current home loan with a new one. The new loan pays off the old loan, and you start fresh with new terms. These terms may include a lower interest rate, a new loan length, or a different type of loan.

Most people refinance to save money or adjust their monthly payments. A lower interest rate can reduce how much you pay over time. A longer loan term can lower your monthly cost, while a shorter term can help you finish faster.

For example, let us say you took a home loan of ₹40 lakh at 9% interest. After a few years, rates drop to 7%. You refinance your loan at the new rate, and your monthly payment becomes lower. Over time, you also pay less interest.

You can also refinance to switch from a variable rate to a fixed rate. This can make your payments more stable. Some homeowners also take extra cash from their home value during refinancing.

The process does not erase your debt. It simply replaces your old loan with a new one that better fits your needs. This basic idea is the foundation of how does refinancing work for most homeowners.

When should you consider refinancing a mortgage?

But how does refinancing work in different situations? Before you decide, it helps to understand the different reasons people refinance their mortgage.

- Interest rates have dropped: You can refinance when market rates fall below your current rate. Even a small drop can lower your monthly payment. Over time, this can lead to big savings on interest.

- Your credit score has improved: A higher credit score can help you get better loan terms. Lenders may offer you a lower interest rate. This can reduce both your monthly payment and total loan cost.

- You want lower monthly payments: Refinancing can reduce your monthly burden. You can do this by getting a lower rate or choosing a longer loan term. This helps if your budget feels tight.

- You want to pay off your loan faster: You can switch to a shorter loan term. This may increase your monthly payment slightly. But it helps you clear your loan sooner and save on interest.

- You want stable payments: If you have a variable-rate loan, your payments may change over time. Refinancing to a fixed rate can make your payments steady. This helps you plan your finances better.

- You need extra cash: You can use refinancing to borrow against your home value. This is often used for home repairs, education, or medical needs. It gives you access to a lump sum amount.

- Your financial situation has changed: If your income has changed, refinancing can help you adjust your loan. You can choose terms that better match your current needs. This can reduce financial stress.

- You plan to stay in your home longer: Refinancing comes with costs like fees and charges. You should plan to stay long enough to recover these costs. This ensures you actually benefit from refinancing.

How do you refinance a mortgage plan? The process explained

Refinancing replaces your current home loan with a new one. The new loan pays off your old loan in full. After that, you continue payments on the new loan based on its terms.

Many people ask, how does refinancing work step by step. The process is easier to understand when broken into clear stages.

Step 1: Check your goal

How does refinancing work based on your goals? Start by knowing why you want to refinance. You may want a lower rate, smaller payments, or a shorter loan term. Some people also want extra cash from their home value.

Your goal will guide the type of loan you choose. It also helps you decide if refinancing is worth the effort and cost.

Step 2: Review your current loan

Look at your current interest rate, monthly payment, and loan balance. Check how many years are left on your loan. This helps you compare your old loan with new offers.

Also, check for any prepayment charges. Some lenders charge a fee if you close your loan early.

Step 3: Check your credit score and finances

Lenders look at your credit score, income, and debt. A higher score can help you get better terms. Stable income also improves your chances of approval.

If your score is low, you may want to improve it first. Even a small improvement can help you get a better rate.

Step 4: Compare lenders and offers

Do not go with the first offer you see. Compare different lenders and their terms. Look at interest rates, fees, and loan features.

Some lenders may offer lower rates but higher fees. Always check the full cost, not just the monthly payment.

Step 5: Apply for the new loan

Once you choose a lender, you submit your application. You will need to share documents like income proof, bank statements, and property details.

The lender will review your application and start the approval process.

Step 6: Property evaluation

The lender may check your home’s current value. This helps them decide how much they can lend. A higher home value can improve your loan terms.

This step ensures that the loan amount matches the property value.

Step 7: Loan approval and offer

If your application is approved, the lender gives you a loan offer. This includes the interest rate, loan term, monthly payment, and fees.

Read all terms carefully before you accept. Make sure the new loan fits your goal.

Step 8: Loan closing and payoff

After you accept the offer, the new loan is finalized. The lender uses this loan to pay off your old mortgage.

From this point, your old loan is closed. You now start paying the new loan based on its terms.

Step 9: Start new repayments

You begin making payments on the new loan. These payments follow the new interest rate and loan duration.

Understanding these stages makes how does refinancing work much easier for first-time borrowers.

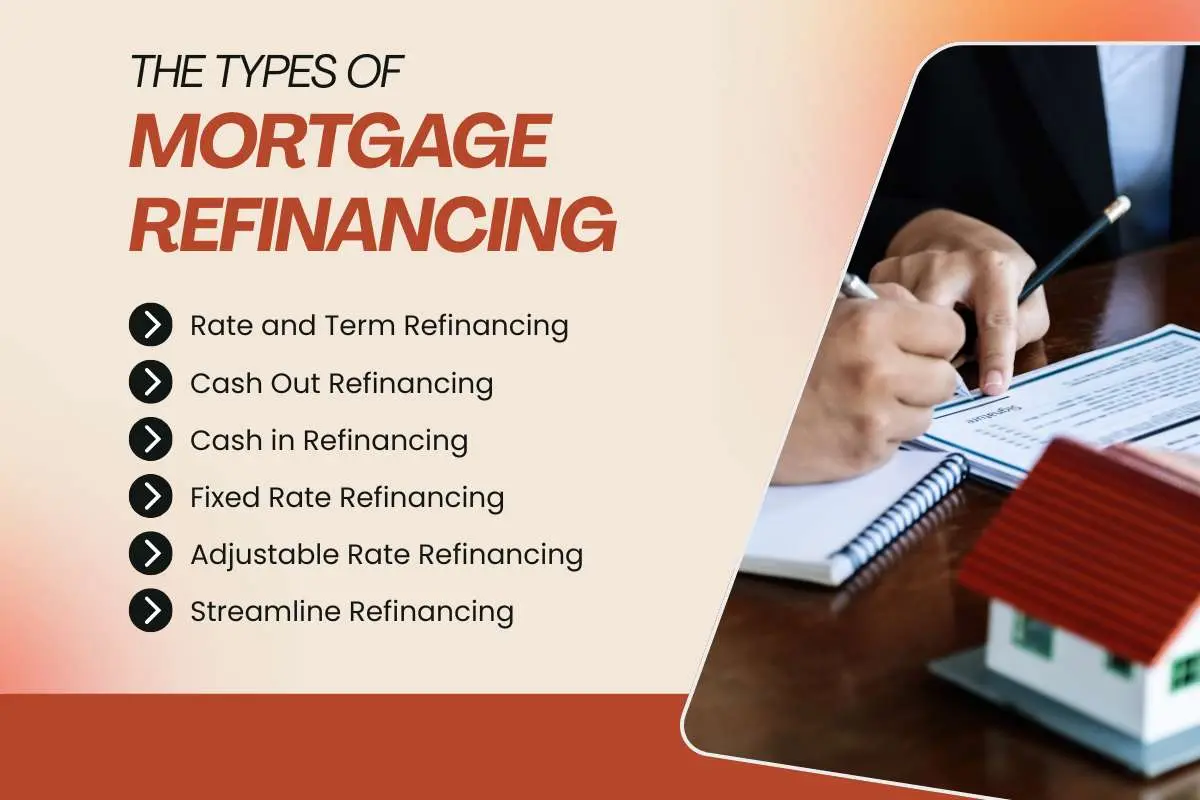

What are the types of mortgage refinancing?

There are different refinancing options, and each serves a different purpose. Knowing these options helps answer the question, how does refinancing work for various financial goals.

1. Rate and term refinancing

This is the most common type of refinancing. You change your interest rate, loan term, or both. The loan amount usually stays the same.

People use this option to get a lower interest rate or adjust their loan duration. For example, you may move from a 20-year loan to a 15-year loan. This can help you save on interest or pay off your loan faster.

2. Cash out refinancing

In this type, you borrow more than what you owe on your current loan. The extra amount is given to you as cash. This money comes from your home’s value.

People often use this for large expenses like home repairs, education, or medical needs. However, your total loan amount increases. This means you may pay more interest over time.

3. Cash in refinancing

This is the opposite of cash-out refinancing. You pay a lump sum amount to reduce your loan balance. Then you refinance the remaining amount.

This can help you get better loan terms or a lower interest rate. It also reduces your monthly payment and total interest cost.

4. Fixed Rate refinancing

This option lets you switch to a fixed interest rate. Your monthly payment stays the same for the entire loan period.

It works well when interest rates are expected to rise. It gives stability and makes budgeting easier.

5. Adjustable rate refinancing

This type moves your loan to a variable interest rate. The rate may start low but can change over time.

People choose this when they want lower initial payments. It can be useful if you plan to sell or repay the loan early. However, payments may increase later.

6. Streamline refinancing

This is a faster and simpler refinancing option. It often requires less paperwork and fewer checks. Some loans may not need a full credit check or property evaluation.

It is usually offered for specific loan types. This makes the process quicker and easier for eligible borrowers.

What are the pros and cons of refinancing a mortgage?

Refinancing can provide major financial benefits, but it also comes with risks and costs. Looking at both sides helps you understand how does refinancing work in real financial situations.

| Pros | Cons |

| A lower interest rate can reduce the total cost | Closing costs and fees can be high |

| Monthly payments may become more affordable | You may extend your loan term and stay in debt longer |

| Helps you pay off your loan faster with a shorter term | A shorter term may increase monthly payments |

| Let’s yo switch to a fixed rate for stable payments | Fixed rates may be higher than current variable rates |

| Gives access to extra cash through home value | Cash-out option increases your total loan amount |

| Can improve cash flow and ease financial stress | Approval depends on credit score and income |

| May help you get better loan terms | You may face prepayment penalties on your old loan |

| Helps adjust the loan based on your current needs | Takes time, paperwork, and effort to complete |

Conclusion:

Refinancing a mortgage often begins with a simple question, but timing plays a bigger role than most people expect. Even small shifts in interest rates or market conditions can change how worthwhile the decision feels. That is one reason why activity can rise or fall quickly.

In fact, the total value of refinance applications dropped by 1.7% for the week ending on April 3, 2026, showing how sensitive homeowners are to changing conditions.

That is why understanding how does refinancing work matters before making a decision.

It helps you look beyond short-term trends and focus on what fits your situation. The right moment to refinance is not just about what the market is doing, but how well the new terms support your goals. When those align, refinancing can turn your mortgage into a tool that works with you, not against you.

FAQs

1. When is the right time to refinance a mortgage?

It often makes sense when interest rates drop, your credit score improves, or you want to change your loan terms. Timing depends on your financial goals.

2. How does refinancing work if I have less equity in my home?

It may still be possible, but options can be limited. Some programs are designed for homeowners with lower equity, depending on eligibility.

3. Can refinancing a mortgage lower my monthly payment?

Yes, if you secure a lower interest rate or extend the loan term, your monthly payment can decrease.