Working capital optimization helps businesses improve cash flow by efficiently managing current assets and liabilities. This guide explains the core components of working capital, the Cash Conversion Cycle (CCC), key financial KPIs, and practical strategies to optimize receivables, inventory, and payables. It also explores the role of technology, common challenges, and emerging trends, helping organizations strengthen liquidity, reduce financing costs, and support sustainable long-term growth.

Many profitable businesses still struggle with one common problem: Cash Flow. The reason isn’t always low sales or rising costs. Often, it’s because cash is tied up in unpaid invoices, excess inventory, or inefficient payment cycles. According to PwC’s 2025 Working Capital Study, the world’s largest companies continue to have hundreds of billions of euros locked in working capital that could otherwise fuel growth, reduce debt, or strengthen day-to-day operations.

That’s why working capital optimization has become a top priority for finance teams and business leaders. Instead of relying on external funding, businesses are finding smarter ways to free up cash already within their operations. Better management of receivables, inventory, and payables can improve liquidity, lower financing costs, and make organizations more resilient during uncertain economic conditions.

In this blog, you’ll learn what working capital optimization is, why it matters, the key components that influence it, and practical ways to improve your working capital ratio. We’ll also look at the metrics, strategies, and technologies that help businesses strengthen cash flow and support long-term growth.

What is working capital optimization?

Working capital optimization is the process of managing a company’s short-term assets and liabilities to improve cash flow and maintain enough liquidity for day-to-day operations. Instead of relying on external financing, businesses focus on freeing up cash already tied up in receivables, inventory, and payables.

Common ways to optimize working capital include collecting customer payments faster, reducing excess inventory, negotiating better supplier payment terms, and improving cash forecasting. These measures help businesses strengthen liquidity, lower financing costs, and support sustainable growth.

Working capital is calculated using the formula:

Working Capital = Current Assets – Current Liabilities

A positive working capital means a business has enough current assets to meet its short-term obligations. However, having too much working capital can indicate idle cash or excess inventory, while consistently negative working capital may point to liquidity issues—unless the business model supports faster cash collections than supplier payments.

While working capital management focuses on monitoring daily financial operations, working capital optimization aims to improve those processes to make better use of available cash and enhance overall financial performance.

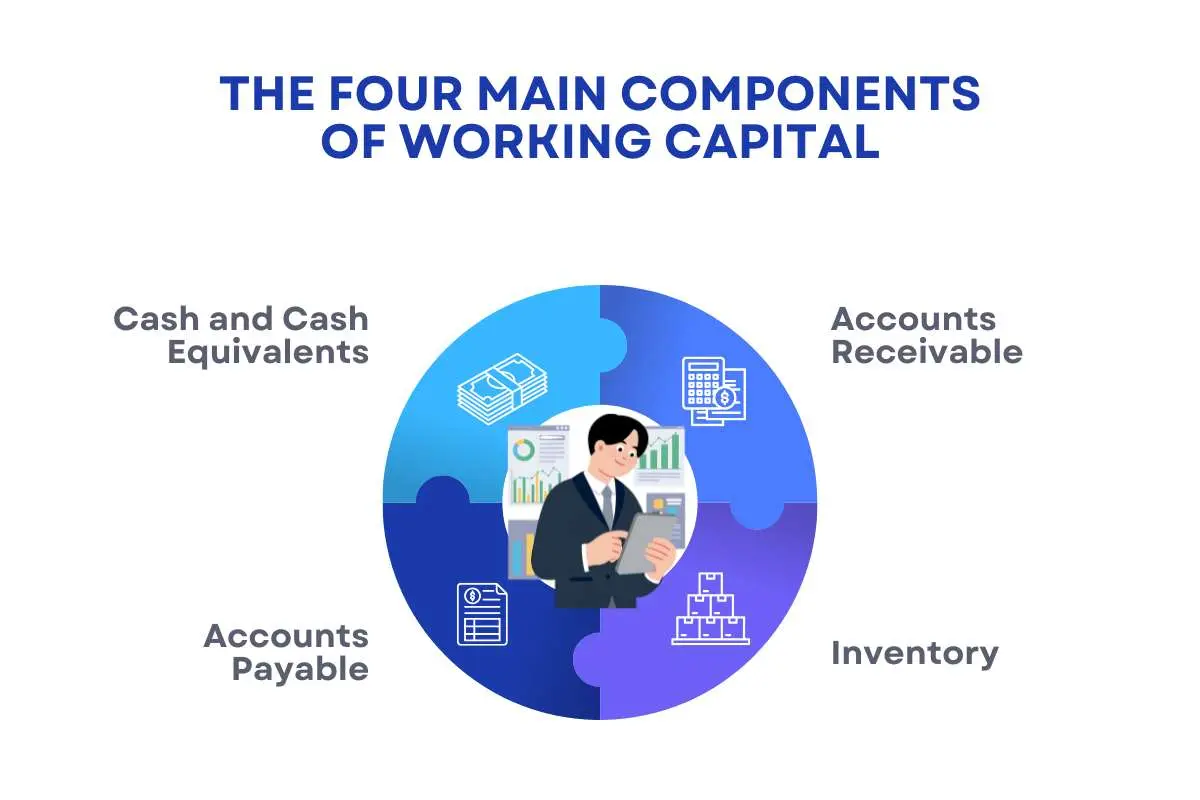

To understand how working capital optimization works, it’s important to first examine its four key components: cash, accounts receivable, inventory, and accounts payable.

What are the four main components of working capital?

Working capital is built on four key components: cash, accounts receivable, inventory, and accounts payable. Together, they determine how efficiently a business manages its cash flow and short-term financial obligations. According to PwC’s 2025 Working Capital Study, businesses still have an estimated €1.84 trillion tied up in excess working capital, highlighting the importance of managing these components effectively.

1. Cash and cash equivalents

Cash is used to meet daily operating expenses, from payroll to supplier payments. The goal is to maintain enough liquidity for smooth operations without leaving excess cash idle.

2. Accounts receivable

Accounts receivable is the money customers owe a business. Faster collections improve cash flow and reduce the need for external financing. Businesses can shorten collection cycles through timely invoicing, clear credit policies, and automated payment processes.

3. Inventory

Inventory includes raw materials, work-in-progress, and finished goods. Holding too much inventory locks up cash and increases storage costs, making accurate demand forecasting and inventory planning essential.

4. Accounts payable

Accounts payable represents the money owed to suppliers. Managing payment terms effectively helps preserve cash while maintaining strong supplier relationships. The focus should be on balancing payment timing rather than simply delaying payments.

These four components are closely connected. Improving receivables, inventory, and payables together helps businesses strengthen liquidity, improve cash flow, and make working capital more efficient.

Is a higher or lower net working capital (NWC) better?

Neither is always better. The ideal level of Net Working Capital (NWC) depends on a company’s industry, business model, and operating cycle. The goal of working capital optimization is to maintain enough liquidity to support daily operations without locking up excess cash.

A higher NWC makes it easier to meet short-term obligations, but if it’s too high, it may indicate:

- Excess inventory

- Slow customer payments

- Idle cash that could be invested elsewhere

A lower NWC isn’t always a concern. Many retailers and e-commerce businesses operate with low or even negative working capital because they receive customer payments before paying suppliers. However, if it’s too low, it can increase liquidity risk and make it harder to meet short-term obligations.

According to PwC’s 2025 Working Capital Study, companies with efficient working capital practices convert cash faster and improve liquidity without relying heavily on external financing.

The key takeaway is simple: the goal isn’t to have the highest or lowest NWC; it’s to maintain the right balance. This allows businesses to manage cash efficiently while supporting long-term growth.

What are the seven cash flow drivers?

Every business generates and uses cash through a few key activities. Understanding these cash flow drivers helps identify where working capital is being tied up and where improvements can be made.

The seven most important cash flow drivers are:

| Revenue Growth | Higher sales can increase cash inflows, but only if customers pay on time. |

| Profit Margins | Stronger margins leave more cash available after covering operating costs. |

| Collection Speed (DSO) | Faster customer payments improve liquidity and reduce cash being stuck in receivables. |

| Inventory Turnover | Selling inventory more quickly frees up cash that would otherwise remain tied up in stock. |

| Supplier Payment Terms (DPO) | Managing payment timing carefully helps preserve cash without harming supplier relationships. |

| Operating Expenses | Controlling day-to-day costs directly affects how much cash the business retains. |

| Capital Allocation | Decisions about investments, debt repayment, and expansion influence overall cash availability. |

These drivers are closely linked to working capital. For example, slow collections, excess inventory, or rising operating costs can quickly create cash flow pressure even when sales are growing.

Research from McKinsey & Company shows that many businesses can unlock significant cash by improving receivables, inventory, and payables rather than relying solely on external financing. This is why leading companies track these drivers closely as part of their working capital optimization efforts.

To manage these drivers effectively, businesses often use one important metric: the Cash Conversion Cycle (CCC), which measures how long it takes for cash invested in operations to return to the business.

Understanding the cash conversion cycle (CCC)

The Cash Conversion Cycle (CCC) measures how long it takes for a business to turn its investment in inventory and operations into cash from sales. Simply put, it shows how efficiently a company manages its working capital.

A shorter cash conversion cycle means cash returns to the business more quickly, improving liquidity and reducing the need for external financing. A longer cycle, on the other hand, may indicate slow collections, excess inventory, or inefficient payment processes.

The Cash Conversion Cycle is calculated using the following formula:

Cash Conversion Cycle (CCC) = Days Sales Outstanding (DSO) + Days Inventory Outstanding (DIO) − Days Payables Outstanding (DPO)

Here’s what each component represents:

1. Days sales outstanding (DSO)

DSO measures the average number of days it takes to collect payments from customers after a sale. A lower DSO generally indicates faster collections and healthier cash flow.

2. Days inventory outstanding (DIO)

DIO shows how long inventory remains in stock before it is sold. Reducing DIO helps free up cash that would otherwise be tied up in unsold goods.

3. Days payables outstanding (DPO)

DPO measures how long a business takes to pay its suppliers. Extending payment terms without affecting supplier relationships can help preserve cash and improve liquidity.

According to J.P. Morgan, optimizing these three metrics is one of the most effective ways businesses can strengthen cash flow and improve working capital without increasing debt. Businesses that regularly monitor their Cash Conversion Cycle are also better equipped to respond to market changes and make informed financial decisions.

The Cash Conversion Cycle doesn’t improve on its own. It requires targeted actions across receivables, inventory, and payables.

Working capital optimization strategies

Improving working capital isn’t about making one big change; it’s about improving several financial processes that influence cash flow. The following strategies can help businesses strengthen liquidity, reduce financing costs, and make better use of available capital.

1. Improve accounts receivable

The faster customers pay, the sooner cash becomes available for business operations. Businesses can improve collections by sending invoices promptly, setting clear credit terms, offering digital payment options, and following up on overdue invoices. Automating the invoicing and collection process can also reduce delays and improve cash flow.

2. Optimize inventory levels

Holding excess inventory ties up cash and increases storage costs. Using demand forecasting, inventory management software, and regular stock reviews helps businesses maintain the right inventory levels while avoiding overstocking or stock shortages.

3. Manage supplier payments strategically

Negotiating suitable payment terms with suppliers allows businesses to preserve cash without affecting long-term relationships. Companies should also evaluate early payment discounts to determine when paying sooner provides greater financial value.

4. Improve cash forecasting

A reliable cash flow forecast helps businesses anticipate future cash needs and avoid unexpected shortages. Regularly reviewing cash inflows and outflows enables better financial planning and supports informed business decisions.

5. Invest in automation

Manual finance processes often slow down collections, payments, and reporting. Automating tasks such as invoicing, payment processing, and cash reporting reduces errors, saves time, and provides better visibility into working capital.

According to J.P. Morgan, organizations that take a proactive approach to receivables, inventory, payables, and cash visibility are better positioned to improve liquidity and support long-term growth. Rather than treating working capital as an accounting measure, successful businesses view it as an ongoing process that strengthens financial performance.

While these strategies form the foundation of effective working capital optimization, technology is making them easier to implement. Modern finance tools now provide real-time visibility, automation, and predictive insights that help businesses manage working capital more efficiently.

Role of technology in working capital optimization

Technology has made working capital management faster, more accurate, and more data-driven. Instead of relying on spreadsheets and manual processes, businesses can now monitor cash flow in real time, automate routine tasks, and make quicker financial decisions.

Here are some of the key technologies driving working capital optimization:

1. Enterprise resource planning (ERP) systems

Enterprise Resource Planning (ERP) platforms bring together financial, inventory, procurement, and sales data into a single system. This gives finance teams a complete view of working capital and helps identify issues before they affect cash flow.

2. Artificial intelligence (AI) and predictive analytics

AI-powered tools analyze historical and real-time data to forecast cash flow, predict customer payment behavior, and estimate inventory demand. This helps businesses make more informed decisions and reduce excess working capital.

3. Treasury management systems (TMS)

Treasury Management Systems provide better visibility into cash positions, bank accounts, and liquidity across the organization. According to J.P. Morgan, greater cash visibility enables businesses to make faster funding decisions and optimize liquidity more effectively.

Research by KPMG shows that organizations using digital finance tools and data-driven forecasting are better equipped to improve cash flow, strengthen liquidity, and respond to changing market conditions.

Key KPIs to measure working capital performance

Improving working capital is only part of the process. Businesses also need to track the right metrics to understand whether their strategies are delivering results. Monitoring these Key Performance Indicators (KPIs) helps identify inefficiencies, improve cash flow, and support better financial decisions.

| KPI | What It Measures | Why It Matters |

| Working Capital Ratio (WCR) | Current assets ÷ current liabilities | Indicates whether a business can meet its short-term obligations. |

| Cash Conversion Cycle (CCC) | Time taken to convert inventory into cash | A shorter cycle means cash is recovered more quickly. |

| Days Sales Outstanding (DSO) | Average time to collect customer payments | Lower DSO improves liquidity and reduces cash tied up in receivables. |

| Days Inventory Outstanding (DIO) | Average time inventory remains in stock | Lower DIO helps free up cash and reduces holding costs. |

| Days Payables Outstanding (DPO) | Average time taken to pay suppliers | Managing DPO effectively helps preserve cash while maintaining supplier relationships. |

| Operating Cash Flow | Cash generated from core business operations | Shows whether daily operations generate enough cash to support the business. |

| Current Ratio | Current assets ÷ current liabilities | Measures short-term financial health and liquidity. |

No single KPI tells the complete story. For example, reducing DSO may improve cash flow, but if inventory remains high, overall working capital efficiency may still suffer. Similarly, extending supplier payment terms can strengthen liquidity, but delaying payments too long could affect supplier relationships.

According to KPMG, businesses that regularly monitor working capital metrics are better positioned to identify cash flow risks early, improve financial planning, and respond quickly to changing business conditions.

Tracking these KPIs consistently allows businesses to make informed decisions rather than reacting to cash shortages after they occur. However, even with the right metrics in place, many organizations face common challenges that prevent them from achieving efficient working capital management. Let’s look at some of the most common obstacles and how they can be addressed.

Common challenges in working capital optimization

Even with the right strategies and performance metrics, many businesses struggle to optimize working capital. Market uncertainty, inefficient processes, and limited cash visibility can all affect liquidity and slow business growth.

Some of the most common challenges include:

1. Delayed customer payments

Late payments are one of the biggest causes of cash flow pressure. When receivables remain unpaid for longer than expected, businesses may need to rely on short-term financing to cover operational expenses.

2. Excess inventory

Holding more inventory than necessary ties up cash and increases storage, insurance, and obsolescence costs. Regular inventory reviews and better demand forecasting can help reduce these risks.

3. Poor cash flow visibility

Without a clear view of cash inflows and outflows, it’s difficult to forecast future cash needs or make informed financial decisions. This often leads to unexpected liquidity gaps.

According to J.P. Morgan, improving visibility across receivables, payables, inventory, and cash positions enables businesses to make better decisions and respond more effectively to changing market conditions.

While these challenges are common, they are also manageable. Businesses that combine strong financial processes with the right technology and regular performance monitoring are better positioned to improve liquidity and build long-term resilience.

Future trends in working capital optimization

As businesses face rising costs, economic uncertainty, and increasingly complex supply chains, working capital optimization is becoming more technology-driven and proactive. Instead of reacting to cash flow issues, organizations are using data and automation to make faster, more informed financial decisions.

Here are some of the key trends shaping the future:

1. AI-powered cash flow forecasting

Artificial intelligence is helping finance teams predict cash inflows and outflows with greater accuracy. Better forecasting allows businesses to plan, reduce cash shortages, and improve decision-making.

2. Greater use of automation

More companies are automating routine tasks such as invoicing, payment processing, and bank reconciliations. This reduces manual effort, minimizes errors, and gives finance teams more time to focus on strategic planning.

3. Real-time financial insights

Modern ERP and Treasury Management Systems provide real-time visibility into cash positions, receivables, payables, and inventory. This allows businesses to identify issues early and respond more quickly to changing market conditions.

Looking ahead, the businesses that succeed won’t necessarily be those with the largest cash reserves; they’ll be the ones that manage cash most efficiently. By combining sound financial practices with modern technology, organizations can improve liquidity, reduce financial risk, and create a stronger foundation for long-term growth.

Conclusion:

Working capital optimization is about making every dollar work smarter. By improving how cash, receivables, inventory, and payables are managed, businesses can strengthen cash flow, reduce financing needs, and improve financial flexibility.

The key is to monitor the right metrics, adopt efficient processes, and make continuous improvements. In a changing business landscape, organisations that actively optimise their working capital are better positioned to manage uncertainty, seize growth opportunities, and achieve long-term financial stability.

FAQs

1. What is the primary goal of working capital optimization?

The primary goal is to improve cash flow by efficiently managing current assets and liabilities while maintaining enough liquidity for daily operations.

2. What is a good working capital ratio?

A working capital ratio between 1.2 and 2.0 is generally considered healthy, though the ideal ratio varies by industry.

3. How does the Cash Conversion Cycle (CCC) impact working capital?

A shorter Cash Conversion Cycle means cash is recovered faster, improving liquidity and reducing the need for external financing.

4. What are the best strategies for working capital optimization?

Key strategies include faster receivables collection, optimizing inventory, managing supplier payments, improving cash forecasting, and automating financial processes.

5. Why is working capital optimization important?

It strengthens cash flow, improves liquidity, lowers financing costs, and supports sustainable business growth.