Liquidity management keeps your business alive. It places cash in the right spots at the right time. Profit shows performance, but quick cash ensures you survive. To stay safe, track your cash flow each week. Balance what you owe with money coming in. Do not rely only on bank credit lines. Smart cash moves let you grow when rivals freeze. Ready funds build your best shield.

So, there is a great company with vast sales, but they have no cash left to pay bills. That scary trap catches many good leaders when the daily cash flow stops. Right now, high interest rates and rapid tech shifts squeeze your cash hard.

A single slip with your funds can shut down your shop for good. True liquidity management means you have cash ready for any cost. It is the lifeblood that keeps your daily business doors wide open.

You cannot afford to guess about your money in times like these. Let us look at how you can shield your cash from these threats.

What is liquidity management and how does it protect your business?

At its core, this practice means putting cash in the right place at the right time. It coordinates your working capital, cash flow timing, and quick obligations to keep you safe. You must balance what you owe with the money coming in each day.

Many people confuse this vital safety metric with high business returns. However, profitability shows how well you perform, while liquidity ensures you survive the year. You can have great paper wealth and still go bust without ready cash.

To build your shield, you can tap both internal and external cash hubs. Your main internal sources include accounts receivable collections and tight inventory control. Meanwhile, external inputs are pooled from bank lines of credit or short-term loans.

Knowing where your money sits lets you move fast during a sudden crunch. Let us look at the main signs that show your cash needs help.

Why does liquidity management matter more than your assets on paper?

A sudden cash freeze drops a heavy iron curtain on daily business tasks. Poor funds flow leads to late pay, which sparks team panic. This delay then causes deep supplier distrust, which sparks a total supply chain freeze.

Next, your financial standing takes a giant hit from this bad chain. Your credit rating drops low, and your bank loans cost much more. You end up spending too much just to fix past financial holes.

Worst of all, you lose your power to grow when cash stays low. You must pass on good firms to buy and skip new markets. Your rivals will jump on those same choices while you stay stuck.

Look at the sad fall of the giant firm Lehman Brothers. They had great assets on paper, but ran out of quick cash.

- The firm held billions of dollars in very slow housing assets.

- They used short-term loans to fund these long-term deals.

- Shaken banks suddenly stopped lending new cash to the firm overnight.

- The team could not sell off their heavy assets fast enough.

That single massive cash run broke the bank and shook the whole world. Their collapse proves that paper wealth cannot save you from a dry well.

We can avoid that dark path by watching for early warning signs. Let us check the red flags that show your cash needs help.

What are the five components of strong liquidity management?

To keep your business safe, you must build a strong cash framework. This system relies on five key gears that must work well together.

1. Cash flow forecasting

This tool lets you see future money trends with clear sight. For example, a retail shop tracks summer sales to plan for winter costs. This step helps you spot a dry spell before it hits your bank.

2. Working capital management

This process keeps your daily funds in a safe and healthy balance. Consider a tech firm that cuts down its stock to free up cash. This choice keeps your money moving instead of sitting on dusty shelves.

3. Short-term financing tools

These options provide quick money when you need it most. Imagine a factory that uses a line of credit to buy raw goods. This tool bridges the gap while you wait for client checks to land.

4. Liquid asset reserves

These funds act as your primary shield against sudden economic shocks. A consulting firm keeps three months of cash in a high-yield account. This fund ensures you can pay your team even if sales drop low.

5. Cycle optimization

Tuning your payables and receivables speeds up your cash inflows. For instance, a vendor gives a small discount for bills paid in ten days. This trick gets cash into your hands weeks ahead of the deadline.

Each mini-system keeps your firm safe from a sudden cash freeze. Let us move on to the top tools that track these funds.

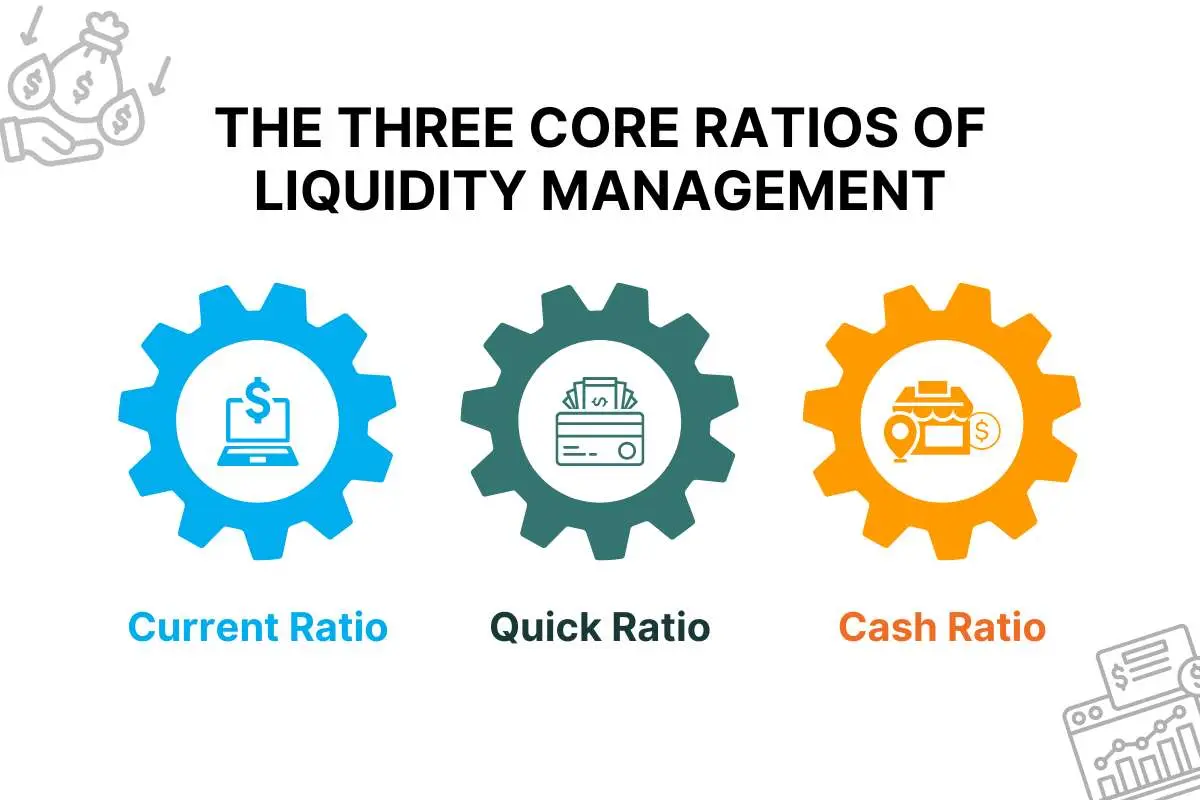

How do you calculate the three core ratios of liquidity management?

To truly know your cash health, you must track your numbers closely. Three key math metrics can show you exactly where your business stands. Though acceptable levels vary by industry and region.

1. Current ratio

This number divides all your short-term assets by your short-term debts. For instance, a safe goal for many firms is a score of two. A low score means you might struggle to pay your bills soon.

Current Ratio= Total Current AssetsTotal Current Liabilities

However, a very high score is not always a good sign either. It often reveals that you have too much idle cash sitting around. You should invest that extra money to grow your firm instead.

2. Quick ratio

This metric strips out your slow inventory to focus only on fast cash. A solid target here is a score of one or more. Service firms can hit this easily since they do not hold stock.

Quick Ratio= Cash+Marketable Securities+Account ReceivablesTotal Current Liabilities

In contrast, a factory might naturally show a much lower score. Their wealth stays locked up in raw goods for months at a time. You must check your own industry norm to judge this number well.

3. Cash ratio

This strict test looks only at your actual cash and quick investments. It shows your power to wipe out all debts this very day. Most steady businesses keep this score around 0.5 or higher.

Cash Ratio= Cash+Marketable SecuritiesTotal Current Liabilities

If this drops too low, a sudden market shock can crush you instantly. Let us see how you can use technology to keep these scores high.

Which smart tools are changing the game for liquidity management today?

Traditional cash forecasting relies on old spreadsheets that look backward at your data. Modern systems use real-time tools to give you an active edge today.

1. AI cash forecasting

Smart code now learns from your past sales and client payment habits. For instance, the system flags a late payer weeks before they default. This tech turns a rough guess into a highly precise roadmap.

2. Real-time treasury dashboards

Old data loops leave leaders blind to sudden global cash shifts. New live feeds track your bank accounts across the globe instantly. You can spot a cash drop and fix it within seconds.

3. Dynamic discounting

This method lets you offer early payouts to suppliers for a discount. Imagine cutting a bill by two percent for a ten-day payout. You save good money while your vendors get quick cash flow.

4. Supply chain finance

You can now link your strong credit line to your suppliers. Banks pay your vendors early based on your high credit score. This move keeps your supply chain stable without draining your funds.

5. Automated liquidity pooling

Holding cash in separate branch accounts wastes your total financial power. Modern software pools all money from your sub-firms into one hub. The system moves funds to dry areas without manual bank wires.

These modern systems shift your cash strategy from defense to rapid growth. Let us wrap up with the best path forward for your business.

How does liquidity management change across different industries?

One size never fits all when you look at different business setups. Each field faces unique hurdles that shape how leaders handle their daily money.

1. Manufacturing

Firms in this space carry heavy raw stock and slow goods conversion cycles. A long gap exists between buying metals and collecting cash from sales. You must tie up a lot of capital just to keep your factory lines running. This setup requires large buffer funds to survive slow invoice collection times.

2. SaaS models

Software subscription setups enjoy very stable and recurring cash inputs every single month. You collect steady fees upfront from users before you deliver the cloud service. This model lowers your cash risks and makes future inflows easy to predict. However, you must track your renewal rates closely to maintain this steady health.

3. Retail trade

Stores face intense seasonal pressure that swings their bank balances up and down. You must spend vast sums to buy winter stock months before shoppers arrive. A bad holiday sales week can wipe out your liquid funds very fast. Your survival relies on matching your short-term debt with tight holiday sales.

4. Banking groups

Financial firms do not just manage cash for growth; they face strict laws. Banks transform short-term customer deposits into very long-term property loans. This basic structure makes them highly vulnerable to sudden runs on the bank. They must follow global rules to hold prime assets against sudden shocks.

A perfect cash plan in one field can cause a rapid crash in another. Let us build a quick summary to help you map your own path.

What common mistakes can ruin your liquidity management strategy?

Even smart teams can fall into blind spots that drain their hard-earned funds. Avoiding these specific mistakes will keep your business well ahead of the pack.

1. Relying too much on credit

Many firms treat a bank line of credit as their primary safety net. This choice leaves you exposed when banks suddenly freeze loans during a crash. You face a sudden halt when you have no actual cash saved.

2. Ignoring old receivables

Leaders often celebrate high sales while invoices sit unpaid for months at a time. Late client payments quickly turn into dead losses that destroy your daily cash. You cannot pay your team with money that only exists on paper.

3. Slow forecasting cycles

Checking your cash flow statement just once a quarter creates a massive hazard. Cash moves too fast today for you to rely on old, stale data. A sudden drop can wipe you out before your next scheduled review.

4. Holding excess idle cash

Keeping too much money in a zero-interest checking account wastes your true power. This cash loses value to inflation instead of funding your future strategic moves. You miss out on great deals when your money sits completely still.

Recognizing these traps helps you build a much stronger and safer system. Let us look at how you can tie all these pieces together.

Are you following this five-step checklist for better liquidity management?

You can build a highly stable cash shield by following five clear steps. This process gives your business a repeatable path to protect its daily funds.

Step I: forecast cash flows: weekly step.

Map out all your expected incoming funds and fixed costs for next month. List your clear customer pay dates alongside your fixed rent and vendor bills. This view shows you exactly when your bank balance will dip low.

Step ii: classify money buffers: monthly step.

Divide your total wealth into clear tiers based on how fast you need it. Keep your primary cash in quick checking accounts for instant bill payments. Place your extra funds in high-yield tools that you can pull next day.

Step iii: optimize your cycle: continuous step.

Shorten the time it takes to turn raw work back into real cash. Offer your clients small discounts if they pay their invoices within ten days. At the same time, ask your vendors for longer terms to hold your funds.

Step iv: set risk thresholds: quarterly step.

Establish strict red lines for your ratios before a cash crunch occurs. For example, flag your team if your cash ratio drops below point five. This early warning gives you time to cut costs or pull loan lines.

Step v: monitor in real-time: daily step.

Connect your bank feeds to a live dashboard to track cash instantly. Review these balances every morning to spot any sudden drops from late payments. Fast data lets you fix a cash hole before it hurts your firm.

Consistently running this framework ensures your firm maintains its financial health through unexpected market shocks.

Conclusion:

Managing your cash is not just a standard chore for your finance team. It is the ultimate tool that lets you move fast when rivals freeze up. True cash strength gives you the power to pivot during a crisis.

Firms that hold ready funds do not just survive the next market crash. They buy up cheap assets and win new clients while others clear out. Your bank balance determines how far and how fast your firm can grow.

In the end, cash flow speed beats paper wealth every single business day. Build your shield now so you can lead the market when tomorrow comes.

People also asked:

1. What is the main objective of liquidity management?

The primary goal is to ensure your firm always has enough cash to pay its daily bills on time.

2. What is the difference between cash management and liquidity management?

Cash management handles daily coin and currency, while liquidity management plans your total short-term assets and debts.

3. Why do companies fail at liquidity management?

Most firms fail because they rely too much on slow inventory or trust late client invoices on paper.