Financial decision-making plays a vital role in achieving long-term financial success for both individuals and businesses. By setting clear objectives, evaluating risks, analyzing alternatives, and following structured frameworks, decision-makers can allocate resources more effectively and avoid costly mistakes. This article covers key decision-making models, financial planning components, corporate finance decisions, and common pitfalls to help build stronger financial outcomes and sustainable growth.

Did you know that nearly 82% of small businesses fail because of poor cash flow management, according to U.S. Bank? At the same time, research by the Financial Industry Regulatory Authority shows that individuals with financial plans are more likely to achieve their long-term financial goals than those who make decisions without a strategy.

Whether you’re running a business, investing for the future, or managing personal finances, every financial choice has a direct impact on growth, profitability, and financial security. This is where Financial decision-making becomes critical. It is the process of evaluating options, assessing risks, and allocating resources to achieve specific financial goals.

In an increasingly uncertain economic environment, relying on intuition alone is no longer enough. Effective Financial decision-making helps individuals and organizations make informed choices, avoid costly mistakes, and maximize long-term value. This guide explores the key principles, frameworks, and strategies that lead to smarter financial outcomes.

What is financial decision-making?

Financial decision-making is the process of evaluating financial options and choosing the course of action that best supports a specific goal. These decisions can range from everyday choices, such as budgeting and saving, to larger commitments like investing, expanding a business, or securing funding.

At its core, financial decision-making involves balancing potential returns against risks while making the most effective use of available resources. Rather than relying on assumptions or emotions, it requires careful analysis of costs, benefits, and long-term consequences.

Financial decisions generally fall into three categories:

- Investment Decisions: Determining where to allocate money to generate future returns.

- Financing Decisions: Choosing how to raise or manage capital, whether through savings, loans, or equity.

- Operational Decisions: Managing day-to-day finances, including budgeting, cash flow, and expenses.

For individuals, effective financial decision-making can lead to greater financial stability, wealth creation, and goal achievement. For businesses, it supports profitability, sustainable growth, and resilience during economic uncertainty.

Simply put, every financial goal, whether personal or professional, depends on the quality of the decisions made along the way. The better the decision-making process, the stronger the financial outcomes are likely to be.

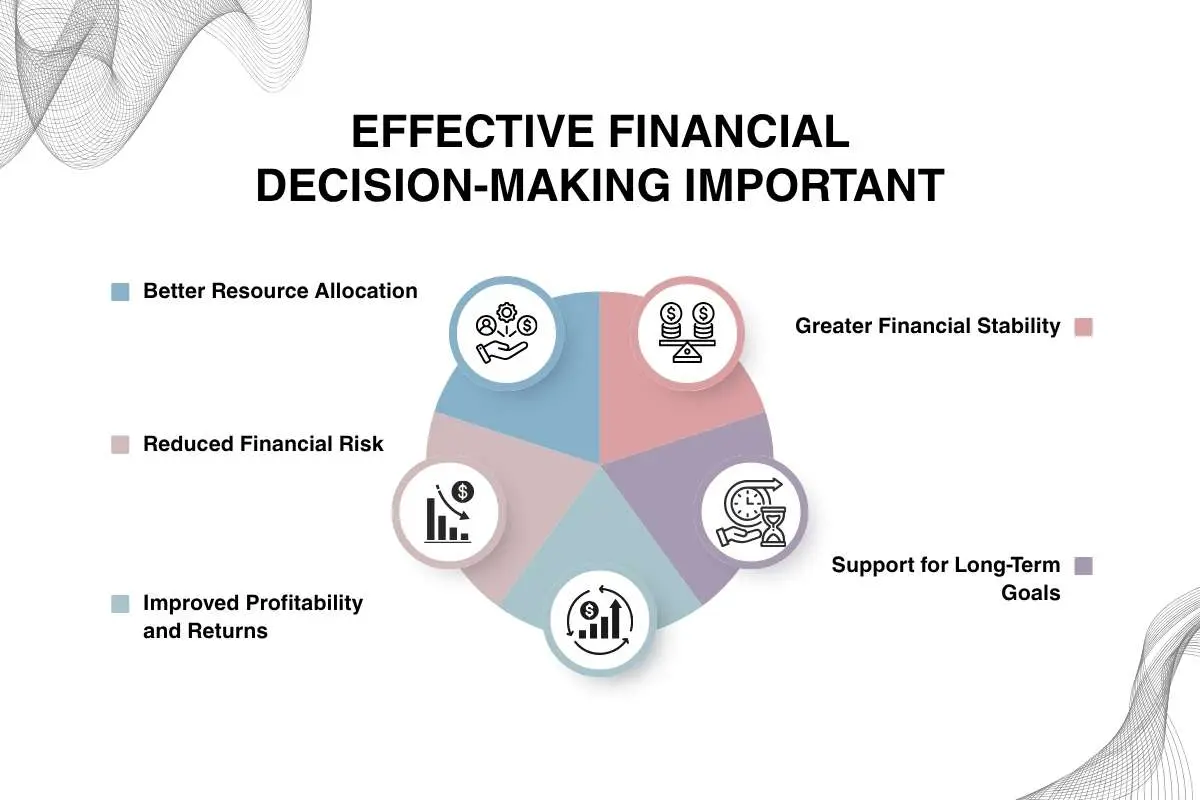

Why is effective financial decision-making important?

Financial decision-making influences virtually every aspect of financial success, from managing daily expenses to achieving long-term growth objectives. Sound decisions help individuals and businesses use their resources efficiently, reduce uncertainty, and create a stronger foundation for the future.

1. Better resource allocation

Resources such as money, time, and capital are limited. Effective financial decision-making ensures these resources are directed toward opportunities that deliver the greatest value. For businesses, this could mean investing in high-growth projects, while individuals may focus on savings, investments, or debt reduction.

2. Reduced financial risk

Every financial choice carries some level of risk. A structured decision-making process helps identify potential challenges before committing resources. By evaluating different scenarios and outcomes, individuals and organizations can minimize losses and make more informed choices.

3. Improved profitability and returns

Businesses that make data-driven financial decisions are often better positioned to improve margins, optimize costs, and increase profitability. Similarly, individuals who make informed investment and spending decisions are more likely to build wealth over time.

4. Greater financial stability

Unexpected economic changes, market fluctuations, or personal emergencies can disrupt financial plans. Strong financial decision-making helps create contingency plans, maintain healthy cash reserves, and improve overall financial resilience.

5. Support for long-term goals

Whether the objective is expanding a business, purchasing a home, funding education, or planning for retirement, achieving major financial goals requires a series of well-informed decisions. Consistent and strategic financial choices increase the likelihood of long-term success.

In short, effective financial decision-making is not just about solving immediate financial challenges; it is about creating sustainable growth, managing risk, and building a secure financial future.

What is the first step in making a financial decision?

Every successful financial outcome begins with a clear understanding of the problem or goal at hand. Therefore, the first step in making a financial decision is defining the financial objective.

Without a clearly identified objective, it becomes difficult to evaluate options, measure success, or determine whether a decision aligns with broader financial priorities. A well-defined goal provides direction and serves as the foundation for the entire decision-making process.

For example, an individual may need to decide whether to invest surplus income, pay off debt, or build an emergency fund. Similarly, a business may be evaluating whether to launch a new product, invest in technology, or expand into a new market. In both cases, the right decision depends on the specific objective being pursued.

When defining a financial objective, it is important to consider:

- The desired outcome

- Available financial resources

- Time horizon for achieving the goal

- Potential constraints or risks

- Expected return or benefit

A clearly defined objective also helps separate needs from wants and prevents decisions from being driven by emotions or short-term pressures. Instead, it creates a framework for evaluating alternatives based on facts and financial priorities.

Once the financial goal is established, the next step is to gather relevant information and explore the available options before making a decision.

The 6-step financial decision-making process

Once a financial objective has been clearly defined, the next step is to follow a structured process for evaluating options and selecting the best course of action. A systematic approach reduces uncertainty, minimizes risk, and increases the likelihood of achieving the desired outcome.

Step 1: define the financial objective

Every financial decision begins with a clear goal. Whether the aim is increasing profits, reducing debt, purchasing an asset, or building long-term wealth, defining the objective provides direction for the entire process.

Step 2: gather relevant information

Good decisions rely on accurate data. This includes collecting information about costs, expected returns, market conditions, available resources, and potential risks. The more relevant information available, the more informed the decision will be.

Step 3: identify available alternatives

Rarely is there only one solution to a financial challenge. At this stage, decision-makers should explore multiple options. For example, a business seeking growth capital may compare bank loans, venture funding, or internal financing before proceeding.

Step 4: evaluate risks and rewards

Each alternative comes with its own benefits and drawbacks. Decision-makers should assess potential returns, financial implications, and associated risks to determine which option offers the best balance between opportunity and uncertainty.

Step 5: make the decision

After analyzing the available alternatives, the most suitable option can be selected. The chosen solution should align with the financial objective while supporting both short-term needs and long-term goals.

Step 6: monitor and review outcomes

Financial decision-making does not end once a choice is made. Outcomes should be tracked regularly to determine whether the decision is delivering the expected results. If circumstances change, adjustments may be necessary to stay on course.

A Practical Example

Consider a small business planning to invest in new software. The company first identifies its objective: improving operational efficiency. It then gathers information about different software solutions, compares alternatives, evaluates costs and expected productivity gains, selects the most suitable platform, and monitors performance after implementation.

By following these six steps, individuals and businesses can make financial decisions that are more strategic, data-driven, and aligned with their long-term objectives.

How do you make a smart financial decision?

Making a financial decision is one thing; making a smart financial decision is another. In an era of economic uncertainty, rising costs, and rapidly changing markets, successful individuals and businesses rely on a combination of data, discipline, and strategic thinking rather than instinct alone.

According to a survey by global analytics firm PwC, organizations that use data-driven decision-making are more likely to report improved financial performance and operational efficiency. The same principle applies to personal finance: informed decisions generally produce better long-term outcomes than emotional or impulsive choices.

Here are five key principles that can help guide smarter financial decisions.

1. Base decisions on data, not emotions

Emotions such as fear, excitement, or overconfidence can lead to poor financial choices. Smart decision-makers focus on facts, trends, and measurable outcomes before committing resources.

Real-life example: During periods of market volatility, many investors panic and sell assets at a loss. In contrast, long-term investors who remain focused on fundamentals have historically been better positioned to benefit from market recoveries.

2. Consider both short-term and long-term impact

A decision that appears beneficial today may create challenges tomorrow. Smart financial choices balance immediate needs with future objectives.

Example: A company may cut employee training costs to reduce short-term expenses, but this could negatively affect productivity and innovation over time. Similarly, an individual who neglects retirement savings may face financial difficulties later in life.

3. Evaluate opportunity costs

Every financial decision involves a tradeoff. Choosing one option means giving up another potential opportunity.

Example: If an entrepreneur invests ₹10 lakh in expanding office space, that capital cannot be used for marketing, product development, or hiring talent. Evaluating opportunity costs helps identify the option with the highest overall value.

4. Assess risks before seeking returns

Higher returns often come with higher risks. Smart decision-makers analyze potential downsides before focusing on expected rewards.

Data point: Historical market data shows that equities have generally outperformed many traditional asset classes over the long term, but they have also experienced significant short-term volatility. Understanding this risk-return relationship is essential when building an investment strategy.

5. Review and adjust regularly

Financial decisions should not remain static. Economic conditions, personal circumstances, and business priorities can change over time. Regular reviews ensure that decisions continue to support financial goals.

Real-life example: Many businesses revisited their budgets and investment plans during the COVID-19 pandemic. Organizations that adapted quickly to changing market conditions were often better equipped to navigate uncertainty and recover faster.

The SMART financial decision framework

Before making any major financial choice, ask yourself:

- Is it aligned with my financial goals?

- Do I have enough data to support the decision?

- Have I evaluated all available alternatives?

- What are the potential risks and rewards?

- Will this decision still make sense in the next three to five years?

If the answer to these questions is yes, you are far more likely to make a financial decision that creates lasting value rather than short-term gains.

Ultimately, smart financial decisions are not about predicting the future perfectly. They are about using the best available information, understanding the tradeoffs, and making choices that support sustainable financial success.

The rule of 5 in decision-making

While there are several frameworks for evaluating financial choices, one of the simplest is the Rule of 5 Decision-Making. The concept encourages individuals and businesses to consider the long-term impact of a decision before taking action by asking a straightforward question:

“Will this decision matter in 5 days, 5 months, or 5 years?”

This approach helps prevent short-term emotions from driving financial choices and encourages a broader perspective on potential outcomes.

How does the rule of 5 work?

When faced with a financial decision, evaluate its consequences across three time horizons:

| 5 Days | What are the immediate effects? |

| 5 Months | How will this decision influence medium-term goals? |

| 5 Years | What is the long-term impact on financial stability and growth? |

By examining each timeframe, decision-makers can better distinguish between temporary concerns and decisions that have lasting financial consequences.

Real-life example: investment decisions

Imagine an investor experiences a sharp market decline and considers selling their portfolio.

| 5 Days | Selling may provide temporary peace of mind. |

| 5 Months | Markets may recover partially, leading to missed gains. |

| 5 Years | Remaining invested could potentially generate significantly higher returns through long-term market growth. |

Looking beyond the immediate situation often leads to more rational and strategic decisions.

Real-life example: business expansion

Suppose a startup is considering investing ₹20 lakh in new technology.

| 5 Days | The expense may strain short-term cash flow. |

| 5 Months | The technology may improve efficiency and reduce operating costs. |

| 5 Years | Increased productivity could strengthen competitiveness and drive sustainable growth. |

Without considering the longer-term perspective, the company might reject an investment that delivers substantial future value.

Why does the rule of 5 matter?

Research in behavioral finance has shown that people frequently place greater emphasis on immediate outcomes than future benefits, a tendency known as “present bias.” The Rule of 5 helps counter this bias by encouraging more balanced thinking.

This framework is particularly useful when making decisions related to:

- Investments

- Major purchases

- Debt management

- Business expansion

- Career and education expenses

The 5-step decision model explained

While the Rule of 5 helps put financial decisions into perspective, complex financial choices often require a more structured approach. This is where the 5-Step Decision Model becomes valuable. Widely used by businesses, investors, and financial planners, the model provides a systematic framework for making informed and objective decisions.

Step 1: identify the problem or opportunity

Every financial decision starts with recognizing a challenge or opportunity that requires action. Clearly defining the issue helps ensure that resources are directed toward the right objective.

Example: A retail company notices declining profit margins despite growing sales. The problem is not revenue generation but increasing operational costs.

Step 2: gather and analyze information

Once the problem is identified, the next step is to collect relevant financial data and market insights. This may include costs, revenues, industry trends, customer behavior, and potential risks.

Data-driven example: Before entering a new market, companies often analyze market size, consumer demand, competitive intensity, and projected returns. This reduces uncertainty and improves decision quality.

Step 3: evaluate alternatives

Rarely is there only one solution. Decision-makers should compare multiple alternatives and assess the financial implications of each option.

Example: A business looking to increase production capacity may consider:

- Purchasing new equipment

- Leasing machinery

- Outsourcing production

- Expanding existing facilities

Each alternative carries different costs, risks, and potential returns.

Step 4: select and implement the best option

After comparing alternatives, the most suitable solution is chosen and executed. The selected option should align with financial goals, available resources, and risk tolerance.

Real-life example: In the early 2000s, Netflix evaluated multiple growth strategies and ultimately chose to invest heavily in streaming technology. Although the decision involved high upfront costs, it transformed the company into one of the world’s leading entertainment platforms.

Step 5: review results and learn

The final step is often overlooked but is critical for long-term success. Monitoring outcomes helps determine whether the decision achieved its intended objectives and provides valuable insights for future choices.

Example: If a company invests in a new marketing campaign, it should track metrics such as customer acquisition costs, revenue growth, and return on investment (ROI). If results fall short of expectations, strategies can be adjusted accordingly.

Why do businesses use the 5-step decision model?

A study by global management consulting firm McKinsey & Company found that organizations that incorporate data and analytics into decision-making are significantly more likely to outperform competitors in profitability and productivity. Structured frameworks such as the 5-Step Decision Model help organizations make decisions based on evidence rather than assumptions.

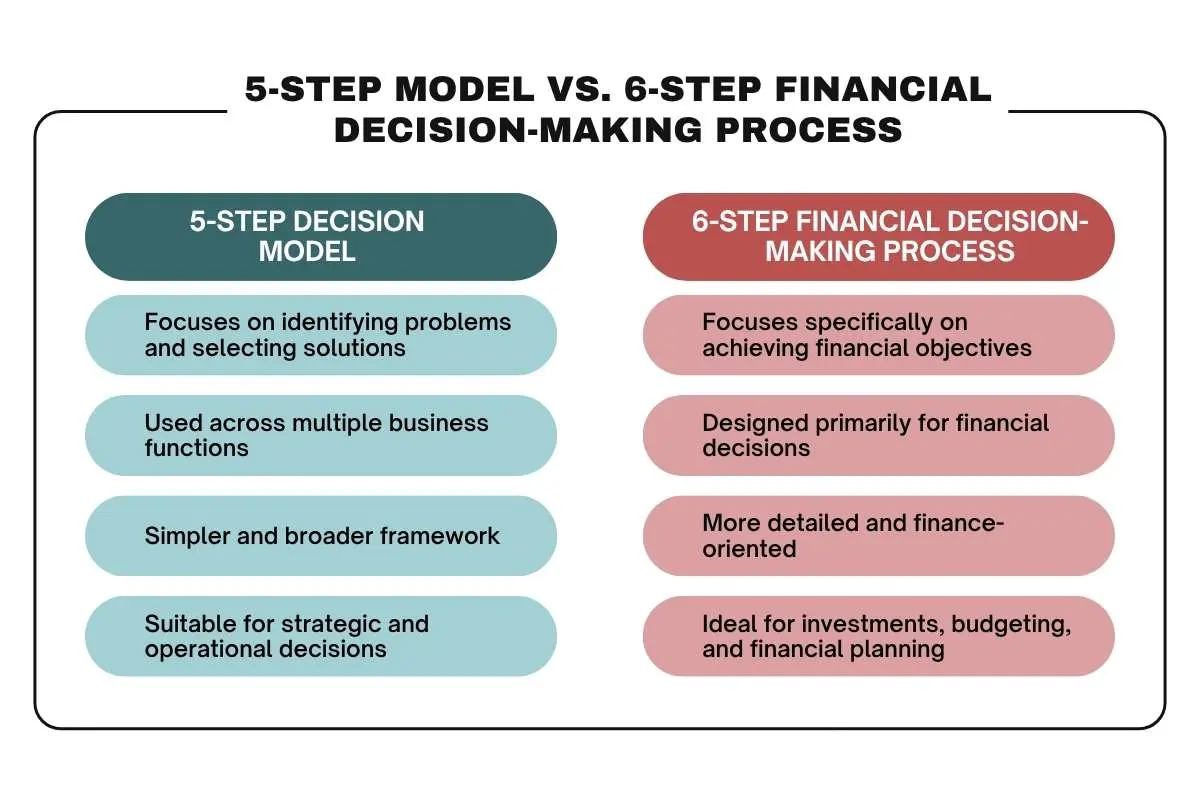

5-step model vs. 6-step financial decision-making process

At first glance, the two frameworks appear similar because both emphasize analysis and evaluation. However, there is a key distinction:

| 5-Step Decision Model | 6-Step Financial Decision-Making Process |

| Focuses on identifying problems and selecting solutions | Focuses specifically on achieving financial objectives |

| Used across multiple business functions | Designed primarily for financial decisions |

| Simpler and broader framework | More detailed and finance-oriented |

| Suitable for strategic and operational decisions | Ideal for investments, budgeting, and financial planning |

Both approaches can improve decision quality, but the choice depends on the complexity and context of the situation.

As financial decisions become more strategic, they often need to fit within a broader financial roadmap. This is where understanding the six key components of a financial plan becomes essential.

The six key components of a financial plan

Making sound financial decisions becomes much easier when they are guided by a well-structured financial plan. Whether for an individual or a business, a financial plan serves as a roadmap that aligns day-to-day financial choices with long-term objectives.

According to a study by the Certified Financial Planner Board of Standards, people who engage in comprehensive financial planning report higher levels of financial confidence and are better prepared to handle unexpected expenses. The same principle applies to businesses, where strategic financial planning helps improve resource allocation, risk management, and sustainable growth.

A comprehensive financial plan typically consists of six key components.

1. Financial goals

Every financial plan begins with clear and measurable goals. These goals provide direction and help prioritize financial decisions.

Examples include:

- Building a retirement fund

- Purchasing a home

- Expanding a business

- Funding higher education

- Achieving financial independence

Real-life example: Many successful companies set specific financial targets such as revenue growth, profit margins, or market expansion goals, which guide their investment and budgeting decisions.

2. Budgeting and cash flow management

A budget helps track income and expenses while ensuring sufficient funds are available for essential needs and future goals.

Why it matters: Research by U.S. Bank has found that cash flow challenges are among the leading causes of business failure. Effective budgeting allows individuals and organizations to control spending and avoid financial shortfalls.

Example: A startup that closely monitors monthly cash flow is better positioned to manage operating expenses and survive periods of slower revenue growth.

3. Emergency planning

Unexpected events such as job loss, medical emergencies, economic downturns, or business disruptions can create significant financial stress.

Financial experts commonly recommend maintaining an emergency fund that can cover several months of essential expenses.

Real-life example: During the COVID-19 pandemic, businesses with stronger cash reserves were generally better equipped to withstand revenue declines and operational disruptions than those operating with minimal liquidity.

4. Investment planning

Investment planning focuses on growing wealth and achieving long-term financial objectives through strategic allocation of capital.

Investment options may include:

- Stocks

- Bonds

- Mutual funds

- Real estate

- Business expansion projects

Data point: Historically, equity markets have outperformed many traditional savings instruments over extended periods, demonstrating the importance of long-term investing for wealth creation.

5. Risk management and insurance

Every financial plan should address potential risks that could undermine financial stability.

This may include:

- Health insurance

- Life insurance

- Business insurance

- Asset protection strategies

- Diversified investment portfolios

Example: A manufacturing company may purchase insurance coverage to protect against equipment damage, operational disruptions, or liability claims that could otherwise result in substantial financial losses.

6. Retirement and long-term wealth planning

Long-term financial security requires planning beyond immediate needs. This component focuses on building assets and generating sufficient income to support future lifestyle goals.

Real-life example: Companies often contribute to employee retirement programs to encourage long-term financial well-being, while individuals may invest consistently in retirement accounts to benefit from compounding returns over time.

How these components work together

Consider a young professional aiming to achieve financial independence. Their goals define the destination, budgeting manages current resources, emergency savings provide security, investments drive wealth growth, insurance reduces risk, and retirement planning ensures long-term financial stability.

Similarly, a business uses these same principles to balance growth opportunities with financial resilience.

Together, these six components create a strong financial foundation, enabling individuals and organizations to make more informed and confident financial decisions. While these elements focus on planning, businesses must also make critical financial choices at an organizational level. These choices are reflected in the four major decisions of the finance function, which play a central role in corporate success.

The four major decisions of the finance function

While personal financial planning focuses on achieving individual goals, businesses face a broader challenge: deciding how to allocate resources to maximize value and ensure long-term growth. At the corporate level, nearly every strategic move from launching a new product to entering a new market depends on four fundamental financial decisions.

These decisions form the backbone of the finance function and directly influence a company’s profitability, liquidity, and market value.

1. Investment decisions

Also known as capital budgeting decisions, investment decisions determine where a company should allocate its financial resources to generate future returns.

Examples include:

- Purchasing new machinery or equipment

- Investing in technology and automation

- Expanding into new markets

- Acquiring another business

- Funding research and development

Real-life example: In 2025, global technology companies continued investing billions in artificial intelligence infrastructure and data centers despite high upfront costs. The objective was clear: position themselves for long-term growth in the rapidly expanding AI market.

Why it matters: Poor investment decisions can drain resources and reduce profitability, while well-planned investments can create sustainable competitive advantages.

2. Financing decisions

Once a company identifies an investment opportunity, it must decide how to fund it. Financing decisions involve selecting the most appropriate mix of debt, equity, and internal funds.

Common financing sources include:

- Bank loans

- Corporate bonds

- Venture capital

- Equity issuance

- Retained earnings

Real-life example: Many startups initially rely on venture capital to accelerate growth, while mature businesses often use retained earnings or debt financing to fund expansion projects.

Data point: According to the World Bank, access to financing remains one of the most significant growth challenges for small and medium-sized enterprises (SMEs) worldwide, highlighting the importance of effective financing decisions.

3. Dividend decisions

Dividend decisions determine how much of a company’s profits should be distributed to shareholders and how much should be retained for future growth.

Companies generally have two options:

- Distribute profits as dividends

- Reinvest profits into the business

Real-life example: Companies such as Apple Inc. and Microsoft Corporation return billions of dollars to shareholders through dividends and share buybacks while continuing to invest heavily in innovation and growth initiatives.

Why it matters: The right balance between shareholder returns and reinvestment can significantly influence investor confidence and long-term business performance.

4. Liquidity decisions

Liquidity decisions focus on managing short-term assets and liabilities to ensure a company can meet its financial obligations when they become due.

This includes managing:

- Cash reserves

- Accounts receivable

- Inventory levels

- Short-term debt

- Working capital

Real-life example: During economic downturns, businesses with strong liquidity positions are often better equipped to continue operations, pay employees, and seize new opportunities than competitors facing cash shortages.

Data point: Studies consistently show that cash flow challenges are among the leading reasons businesses struggle or fail, making liquidity management a critical component of financial success.

How these decisions work together

Consider a manufacturing company planning to open a new production facility:

| Investment Decision | Should the company build the facility? |

| Financing Decision | Should it use a loan, issue equity, or use retained earnings? |

| Dividend Decision | Should profits be retained to support expansion? |

| Liquidity Decision | Can the company maintain sufficient cash flow during construction and operation? |

Each decision influences the others, demonstrating why financial management requires a holistic approach rather than isolated choices.

The strategic importance of financial decisions

The most successful organizations understand that growth is not simply about generating revenue; it’s about making smart decisions regarding investments, financing, shareholder returns, and liquidity. Together, these four finance functions provide the framework for sustainable profitability and long-term value creation.

However, even with structured frameworks and financial plans in place, decision-makers can still make costly mistakes. Understanding the most common financial decision-making pitfalls is essential for avoiding unnecessary risks and improving outcomes.

Common financial decision-making mistakes to avoid

Even the most experienced investors, entrepreneurs, and business leaders make financial mistakes. In fact, many financial setbacks occur not because of a lack of opportunities but because of poor decision-making. Understanding these common pitfalls can help individuals and organizations make more informed choices and avoid costly consequences.

1. Making decisions based on emotions

Fear, greed, and overconfidence are among the biggest enemies of sound financial decision-making. Emotional reactions often lead to impulsive choices that overlook facts and long-term objectives.

| Example | During periods of market volatility, many investors sell assets out of fear, locking in losses. Conversely, during market booms, some investors take excessive risks in pursuit of quick gains. Both behaviors can negatively impact long-term wealth creation. |

| Key takeaway | Let data, research, and financial goals, not emotions, drive decisions. |

2. Failing to conduct adequate research

Making financial decisions without gathering sufficient information increases the likelihood of errors. Whether investing in a stock, purchasing a property, or launching a business initiative, due diligence is essential.

| Example | A company expanding into a new market without analyzing customer demand, competition, and regulatory requirements may face unexpected costs and lower-than-expected returns. |

| Key takeaway | The quality of a financial decision is often determined by the quality of the information behind it. |

3. Ignoring risk assessment

Many decision-makers focus heavily on potential returns while underestimating the associated risks. This imbalance can expose individuals and businesses to significant financial losses.

| Example | The 2008 global financial crisis highlighted the consequences of inadequate risk assessment, as many institutions underestimated the risks associated with complex financial products. |

| Key takeaway | Always evaluate both the upside potential and the downside risk before committing resources. |

4. Overlooking opportunity costs

Every financial decision involves a tradeoff. Choosing one option means giving up another potential opportunity.

| Example | A business that allocates a large portion of its budget to office expansion may have fewer resources available for product development, hiring, or marketing initiatives. |

| Key takeaway | Consider what you may be sacrificing before making a financial commitment. |

5. Focusing only on short-term gains

Short-term thinking can undermine long-term financial success. Decisions that provide immediate benefits may create larger challenges in the future.

| Example | Companies that reduce investments in innovation or employee development to improve quarterly profits may struggle to remain competitive over the long run. |

| Key takeaway | Balance immediate financial needs with future growth objectives. |

Lessons from successful decision-makers

Many of the world’s most successful investors and business leaders share a common trait: they prioritize discipline, patience, and informed analysis over speculation and emotion. Their success is often the result of consistently avoiding the mistakes that derail others.

By recognizing these common pitfalls, individuals and organizations can strengthen their financial decision-making process, improve risk management, and make choices that support long-term financial success.

While understanding mistakes is important, seeing how sound financial decision-making works in practice can be even more valuable. Examining real-world examples provides practical insights into how effective financial choices create lasting results.

Conclusion:

Financial decision-making is more than choosing between financial options, it’s a strategic process that shapes long-term success. Whether managing personal finances, evaluating investments, or leading a business, the quality of financial decisions directly influences growth, profitability, and financial stability.

As the examples of Amazon, Netflix, Apple, and Warren Buffett demonstrate, successful outcomes rarely stem from luck. They are built on clear objectives, data-driven analysis, careful risk assessment, and disciplined execution. By following structured frameworks such as the 6-Step Financial Decision-Making Process, understanding the key components of a financial plan, and avoiding common decision-making mistakes, individuals and organizations can make more confident and effective financial choices.

In an increasingly complex financial landscape, those who consistently make informed decisions are better positioned to manage uncertainty, seize opportunities, and achieve their long-term goals. Ultimately, strong financial decision-making is not just a financial skill, it is a competitive advantage.

FAQs

1. What is financial decision-making?

Financial decision-making is the process of analyzing financial options and selecting the best course of action to achieve specific financial goals.

2. Why is financial decision-making important?

It helps individuals and businesses allocate resources efficiently, minimize risks, and improve long-term financial outcomes.

3. What is the first step in financial decision-making?

The first step is defining a clear financial objective or identifying the problem that needs to be solved.

4. What are the four major financial decisions in business?

The four major decisions are investment, financing, dividend, and liquidity decisions.

5. How can I make better financial decisions?

Set clear goals, gather relevant data, evaluate alternatives, assess risks, and regularly review your decisions to ensure they remain aligned with your objectives.