Smart working capital management keeps your business safe. It helps you track cash, stock, and bills every day. Good tracking helps you pay workers on time. It also stops sudden cash shortages. You should collect customer payments fast. Then, you can delay vendor payments to maintain liquidity. This simple balance helps your company grow well.

Working capital management feels like a buzzword thrown around in a Q4 meeting. And honestly, it is. But once you understand the use of this “buzzword,” you are able to relax a bit about your organization’s financial worries.

So, what is it? How does it work? What are its components? We will look at all of that today.

WCM is a process of managing short-term assets and liabilities to maintain liquidity. In this blog, we will see how it works and how you can apply it in your company.

So, let’s begin, shall we?

What is working capital management?

We look at what we own and what we owe right now. We subtract current liabilities from current assets to find the total sum. This simple math formula shows us the money we can spend today.

Working Capital = Current Assets – Current Liabilities

Current assets are things we can turn into cash very fast. This part includes bills, bank funds, and items on the shelf. Current liabilities are the debts we must pay off within a year. They are the bills from vendors and short-term loans we owe.

We use these funds for short-term operational funding needs. This cash keeps the lights on and pays your staff on time.

You might think this sounds just like simple liquidity management work. But liquidity management only looks at cash on hand for quick bills. Working Capital Management goes much deeper into all parts of the daily loop.

A small business handles this task in a very simple way. They just watch daily sales to see what cash they have left. A giant firm needs a big team to track every single coin. They must plan months in advance to stay safe from major risks.

Now you know the basics of how we check this cash. Let us move on to see how this system works next.

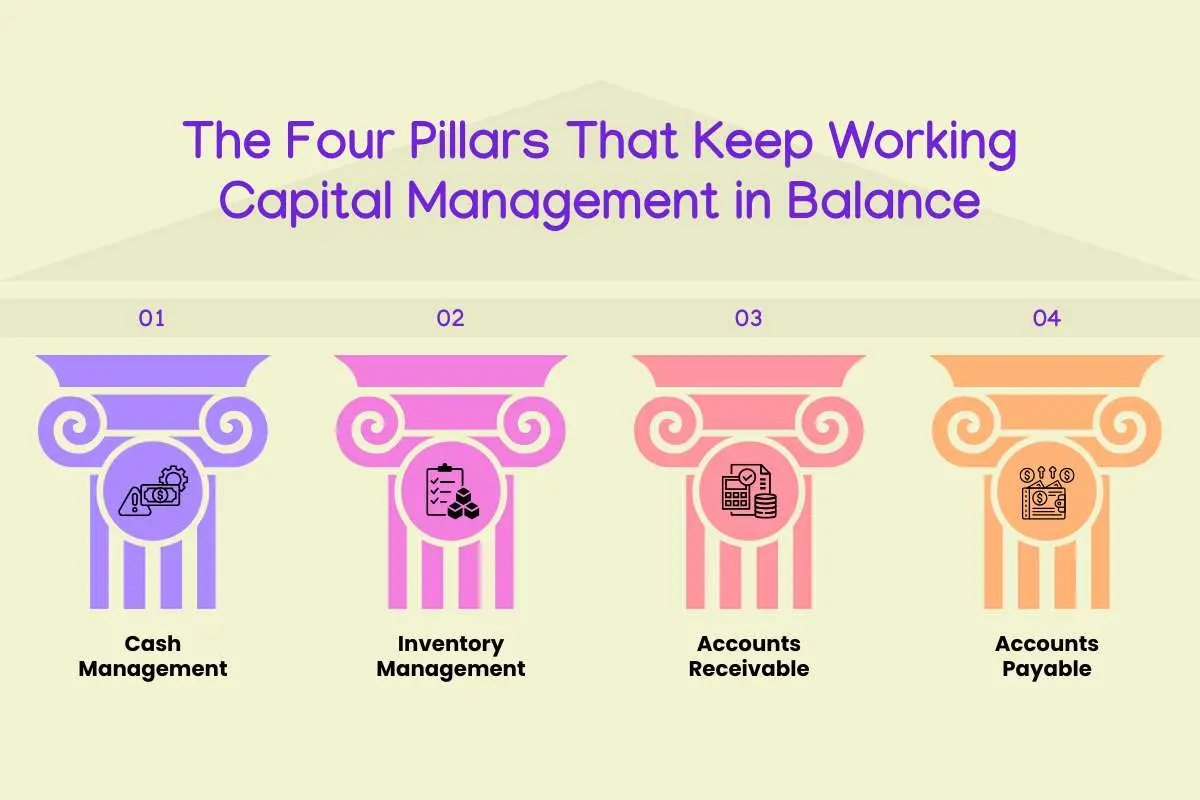

The four pillars that keep working capital management in balance

We must look at the key parts that make this system work. Let’s break this down into four core fields we track each day.

1. Cash management

We need to know how much cash flows in and out now. So, we use cash forecasting to predict our income for next month. These steps help us map out our spending with no big surprises.

We also keep extra money on hand for a rainy day. These emergency reserves protect us if our sales drop off out of nowhere. We stay safe when we plan for things we do not expect.

2. Inventory management

We have to find a sweet spot for the goods we store. Overstocking risks mean we tie up too much cash in stock. We pay high fees to store items that just sit on shelves.

On the flip side, we must avoid stockouts at all costs. If we run out of goods, we cannot serve our buyers. They will leave us and buy from a rival shop instead.

3. Accounts receivable

We must watch the money that our clients owe us. We set firm customer credit policies before we sell our goods. We only give credit to folks who pay bills on time.

We also work hard to shorten our collection cycles each month. We want buyers to pay us back as fast as they can. Fast payments keep our bank account full and ready for use.

4. Accounts payable

We also have to manage the money we owe to vendors. We must plan our supplier payment timing with a lot of care. No one likes to pay too early and lose cash.

But we still pay on time to maintain great supplier relationships. Good bonds with vendors mean we get better deals down the road. We win when we treat our partners with real respect.

Component impacts

We made this quick list to show what happens with bad balances. Most guides skip this view, but it helps us see the risks.

| Component | What Happens If Too High | What Happens If Too Low |

| Cash Management | Your funds sit idle and earn no extra money for you. | You face a high liquidity risk and cannot pay bills. |

| Inventory Management | Your storage costs rise because old stock sits on shelves. | You suffer from lost sales when items run out fast. |

| Accounts Receivable | You get delayed cash because clients take too long to pay. | You lose customers because your credit terms are strict. |

| Accounts Payable | You face supplier issues and lose trust in your vendors. | You feel a heavy cash strain from paying bills too fast. |

Now we see the four parts that we must balance well.

The cash flow mistakes that create working capital headaches

We can run into big bumps if we do not watch our cash. We see five major blocks that trip up most business teams.

1. Slow customer payments

We face a hard time when buyers take too long to pay. Slow customer payments mean our cash sits in their bank accounts. We cannot buy new stock when our own funds are stuck there.

We must watch our rising receivable days as a clear warning sign. If this number climbs, a working capital crisis might start soon. We need to chase down those late bills right away.

2. Excess inventory

We hurt our cash flow when we buy too many goods. Excess inventory locks up our money in boxes on a shelf. This stock just sits in the back and gathers dust for months.

We waste cold cash on storage space we do not really need. Look out for stock that moves slowly or does not sell well. That is a major clue that you have tied up too much wealth.

3. Poor cash flow forecasting

We get hit by bad surprises when we do not plan well. Poor cash flow forecasting leaves us blind to our future needs. We cannot guess what we will spend if we do not track trends.

Falling cash reserves are the first early indicator of this huge trap. If our bank balance drops each week, we have a problem. We must fix our math before we run out of funds.

4. Seasonal demand fluctuations

We see our sales go up and down throughout the year. Seasonal demand fluctuations can catch us off guard if we stay lax. We might have high costs during months when sales are low.

We need extra short-term operational funding to get through slow times. If we do not prepare, we will feel a massive pinch. We must save cash from peak times to survive the drops.

5. Rapid growth challenges

We can get hurt even when our firm expands very fast. Rapid growth challenges pop up when we take on too much work. We must spend cash on new staff before clients pay us.

Increased short-term borrowing is a sign that growth costs too much. If we rely on quick loans, our debt will pile up fast. We must pace our wins so we do not break the bank.

Now we know the hazards that can ruin our daily flow. Let us see how we can fix these issues next.

Is your working capital management strategy helping or hurting growth?

We can use smart tools to fix our cash flow blocks now. You can use five modern paths to keep our funds on track.

1. Improve receivables collection

We must speed up the ways we collect cash from buyers. Many use predictive analytics to spot clients who might pay late. This tech tells us which accounts need our focus right away.

We can also offer dynamic discounting to get our cash faster. We give a small price cut if they pay within ten days. This win-win step keeps our bank accounts full and healthy.

2. Automate financial processes

We waste too much time when we do tasks by hand. Companies rely on modern automated software to track their daily bills. This tech sends out quick reminders to buyers who owe us money.

We cut down on human errors and speed up our loop. Your team can focus on growth instead of chasing paper trails. Smart tools do the heavy lifting for us every single day.

3. Optimize inventory levels

We need to keep just the right amount of stock handy. You can use real-time dashboards to check our supply levels now. This view shows us exactly what sells and what sits still.

We can order new goods just when we need them most. We do not waste money on extra storage space anymore. Our cash stays free because we only buy what moves fast.

4. Negotiate better supplier terms

You should talk to vendors to get better deal paths. Always ask for more time to pay your big bills each month. This step lets us keep our cash for a longer time.

You can also use your good payment history to get perks. Vendors will give us better terms when they trust your firm. We build strong bonds that help both sides save money over time.

5. Build cash flow forecasts

We must look ahead so we do not hit bad snags. Use AI-driven forecasting to map out your future income. This math counts past trends and market shifts to stay precise.

We can see cash drops months before they even happen today. This clear view lets us make smart choices with zero panic. We stay ahead of the game because we know the future path.

We now have the tools to manage daily cash well. Let us wrap up what we learned about this system today.

Four essential ratios for measuring working capital performance

Working capital management requires constant tracking with the right math tools. Four main metrics help check short-term business safety.

1. Current ratio

This math tool checks short-term safety for a business. Dividing current assets by current liabilities gives this core score. The metric shows if a firm can pay its bills.

A score between 1.5 and 2.0 is believed to be a healthy benchmark range. A low score means the firm faces a major risk. A high score means cash sits idle with no growth. Though benchmarks vary by sector because inventory intensity, receivable cycles, and supplier terms differ across retail, manufacturing, SaaS, and construction.

2. Quick ratio

A stricter test drops slow stock from the safety check. Quick cash assets divided by current debts give this sharp view. It shows bill coverage with zero reliance on stock sales.

This score typically should stay above 1.0 at all times. A score below 1.0 means stock reliance is too high. A sudden sales drop could cause a massive cash crunch. Though it may vary from industry to industry.

3. Cash conversion cycle

The cash conversion cycle, or CCC, measures time in days. This tool tracks how fast cash moves through the loop. A short cycle keeps a business lean and highly liquid.

Cash Conversion Cycle = Inventory Days + Receivable Days – Payable Days

Three distinct parts make up this core time metric:

- Inventory Days: This score shows how long goods sit on shelves.

- Receivable Days: This part tracks how fast customers pay their bills.

- Payable Days: This counts the time taken to pay company vendors.

Adding stock days and client days, then subtracting vendor days, gives the CCC. A low number means cash returns fast to the bank. Healthy ranges depend a lot on the specific industry type.

4. Working capital turnover ratio

This final metric reveals how hard cash works for a firm. Dividing net yearly sales by average working capital gives the sum. It shows the revenue each dollar of capital creates.

A higher score is generally better for most business setups today. It proves that a firm uses cash in a lean way. A low score means funds go to tasks that lag.

Metric benchmark

This simple table helps check company financial scores with ease. These target ranges keep operations on a safe and steady path.

| Metric | Healthy Range | Practical Meaning |

| Current Ratio | 1.5 to 2.0 | A sufficient cushion exists to pay short-term debts easily. |

| Quick Ratio | Above 1.0 | Fast bills get covered without selling any store stock. |

| CCC | Industry dependent | A lower number means cash returns to the bank faster. |

| Turnover Ratio | Higher is better | Capital works hard to create big sales for the firm. |

These ratios give a clear picture of operational cash flow success.

Real-world working capital management success and failure stories

Real-world examples prove how cash flow choices shape business outcomes. Strong cash management drives growth, while poor control leads to swift failure.

Success cases

1. Apple inc.

This tech giant uses a negative cash conversion cycle strategy. The firm delays supplier payments but collects customer cash very fast. Advanced supply chain steps also keep inventory levels down to a minimum.

As a result, money arrives before bills must be paid off. This loop creates massive cash reserves for the global firm today. Operations remain highly profitable with zero short-term funding stress.

2. Dell technologies

A build-to-order model transformed computer production in the nineties. Customers must place orders and pay for PCs before assembly starts. Dell produces laptops only when needed to cut down on storage.

This just-in-time method minimizes inventory costs for the firm. Unsold stock is avoided, and advance payments shorten the cash loop. The strategy enabled rapid expansion across the global computer market.

3. Walmart

This retail giant introduced a smart system called cross-docking. Goods move fast from trucks to store shelves with zero storage. The firm also negotiated much longer payment terms with global suppliers.

Cash from daily sales arrives long before vendor bills come due. These free funds go straight into new store expansion and tech. A resilient financial structure keeps prices low for shoppers every day.

4. Tesla

An innovative pre-order strategy funded major factory scaling in 2017. The Model 3 car launched with a required advance deposit. This step brought in over four hundred million dollars before work started.

Just-in-time manufacturing also helps reduce holding costs each month. Advance cash flow pays for parts and keeps debt levels low. This financing path shows how smart planning drives rapid industrial growth.

5. Unilever

Advanced demand forecasting helped navigate recent global health supply shocks smoothly. The firm provided early payment solutions to small, vital suppliers. At the same time, it extended terms for its own payments.

These steps maintained liquidity and kept production lines running with ease. Product availability stayed high during times of intense consumer demand peaks. Strong supply chain bonds protected the brand from major market risks.

Failure cases

6. Toys “R” Us

Heavy debt financing created massive interest payments for this toy brand. Poor inventory choices led to excess stock during slow retail months. Shortages then hit shelves right during the peak holiday shopping rush.

Delayed supplier payments damaged vendor bonds and cut off hot items. Strong sales could not save the firm from poor daily cash control. These working capital flaws contributed directly to the 2017 bankruptcy filing.

7. Nokia

This mobile phone brand tied up too much cash in unsold stock. The firm failed to adapt fast as smartphones changed the market. Slow inventory turnover locked up wealth that was needed for tech updates.

Weak cash management limited the ability to innovate and stay ahead. Revenues dropped fast while fixed costs remained a heavy operational burden. This financial trap accelerated the loss of global market dominance.

Future trends in working capital management

Corporate liquidity shifts fast as new tech alters how firms track money. Two major trends dominate the near future of cash management systems.

Agentic AI and automation

Modern software now turns daily cash tracking into a self-optimizing loop. Agentic AI tools continuously sense financial risks across the global supply chain. This tech triggers real-time actions without any slow manual steps.

Automated platforms send instant collection alerts to late-paying clients right away. They also adjust pricing terms dynamically to keep the bank loop safe. Firms no longer rely on slow month-end reviews to protect liquidity.

Structural optimization over short-term levers

Top finance leaders now reject brief, temporary fixes for their cash cycles. Lasting balance sheets require structural changes embedded directly into daily operations. Firms must build deep, end-to-end visibility across all corporate departments.

Predictive tools calculate the exact supply needs to stop harmful inventory spikes before they start. Closer collaboration with suppliers helps create balanced, mutually beneficial commercial terms. True financial resilience comes from smart technology paired with durable workflow updates.

These developments prove that daily cash control has become a highly strategic tool.

Conclusion:

Effective working capital management remains the ultimate foundation for sustainable corporate growth. Balancing short-term assets against operational debts keeps a business safe from sudden market drops. True financial strength combines high liquidity with strict day-to-day operational efficiency.

Firms must focus on constant cash flow optimization to protect thin profit margins. Embracing rapid technology adoption provides the clear insights needed to spot big risks early. Automated dashboards and predictive metrics help management teams make smart, fast choices.

Static financial habits can easily ruin even the most profitable global brands. Success requires absolute clarity over every single moving cent in the transaction loop. Leaders must continuously upgrade their daily systems to survive changing economic environments.

People also asked:

1. What is working capital management?

This process tracks a company’s short-term assets and debts to ensure smooth daily operations. It monitors cash, stock, and vendor bills to keep the business running safely.

2. What is a good working capital ratio?

A current ratio between 1.5 and 2.0 is generally healthy for most firms. This range proves a company can cover near debts without leaving cash idle.

3. How can businesses improve working capital?

Teams can speed up customer collections and optimize their warehouse stock levels. Negotiating longer payment terms with suppliers also keeps cash in the bank longer.

4. Why is working capital management important?

Proper control prevents sudden cash crunches and protects the firm from bankruptcy risks. It ensures the business always has enough funds to pay its workers and bills.