Accounts payable represent what your company owes suppliers, while accounts receivable represent the money customers owe you. This guide breaks down the core structural differences between these two cash flow cycles. You will master liquidity management, learn to balance cash cycles, and discover automation strategies to optimize your corporate working capital immediately.

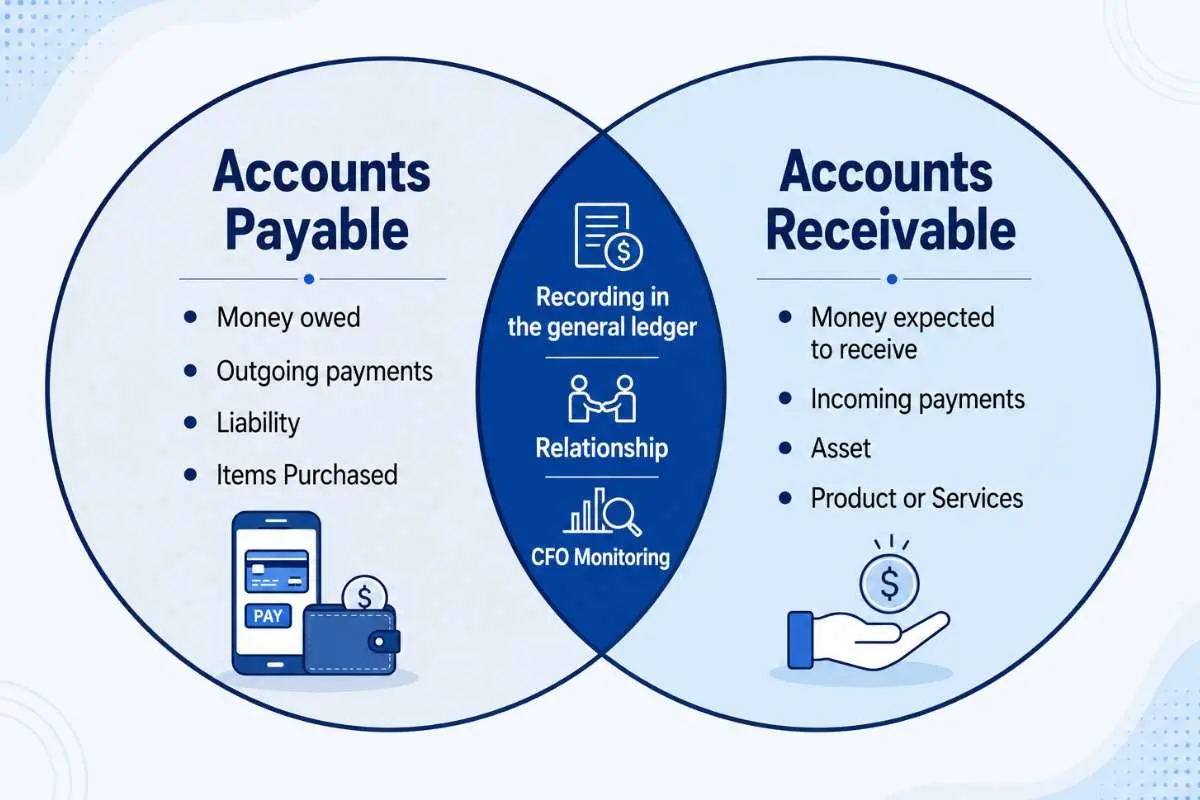

When you analyze accounts payable vs accounts receivable, you unlock the secret to corporate liquidity management. At the most fundamental level, these two categories represent opposite sides of the same cash flow coin.

Accounts payable (AP) means the short-term money your business owes to suppliers for goods or services you bought on credit. Accounts receivable (AR) means the short-term money your customers owe to your business for products or services you sold to them on credit.

AP represents a mandatory future cash outflow, while AR represents an expected future cash flow. Balancing these two cycles prevents sudden corporate insolvency and keeps your business running smoothly.

What are the core structural differences in accounting?

Understanding the fundamental rules of accounts payable vs accounts receivable determines how you track financial health on a company’s balance sheet. They belong to completely different ledger categories.

1. Accounts payable: The short-term credit liabilities

When your procurement team buys inventory or office supplies on credit, the vendor sends you an invoice. Your accounting team immediately logs this amount under accounts payable. AP serves as a current liability because you must pay this debt quickly, typically within 30, 60, or 90 days. Efficient AP teams track these due dates to keep cash in the corporate bank account for as long as possible without damaging relationships with vendors.

2. Accounts receivable: The uncollected revenue assets

When your sales team sells a product or an annual software subscription to a corporate client on credit, you extend that client a line of credit. Your billing system generates an invoice. Until the client actually transfers the money to your bank account, your records track that balance under accounts receivable. AR serves as a current asset because it represents real economic value that will convert into liquid cash within a year.

How do payables and receivables impact the corporate balance sheet?

Comparing accounts payable vs accounts receivable on a balance sheet reveals how your business cycles working capital. Accountants use opposite debit and credit entries to manage these accounts.

| Accounts Payable (AP) | Financial Dimension | Accounts Receivable (AR) |

| Current Liability (Debts due within one year) | Balance Sheet Category | Current Asset (Resources converting to cash within one year) |

| Upcoming cash outflow (Money leaving the business) | Cash Flow Velocity | Expected cash inflow (Money entering the business) |

| Corporate procurement and purchasing | Core Operational Driver | Sales and revenue generation |

| Pay strategically to maintain cash cushions | Management Goal | Collect quickly to fuel daily operations |

| Supply chain disruption and late payment penalties | Primary Financial Risk | Bad debt write-offs and customer defaults |

The dynamic relationships of accounts payable vs accounts receivable create different balance sheet impacts. When your business buys raw materials on credit, the accountant credits accounts payable, which increases your total liabilities. When you pay the vendor via an electronic funds transfer, the accountant debits accounts payable, which reduces your liabilities, and credits your cash account.

For your receivables, the process reverses. When you make a credit sale, the accountant debits accounts receivable to increase your current assets. Once the client settles their bill via an ACH transfer, the accountant debits cash and credits accounts receivable, clearing the asset ledger.

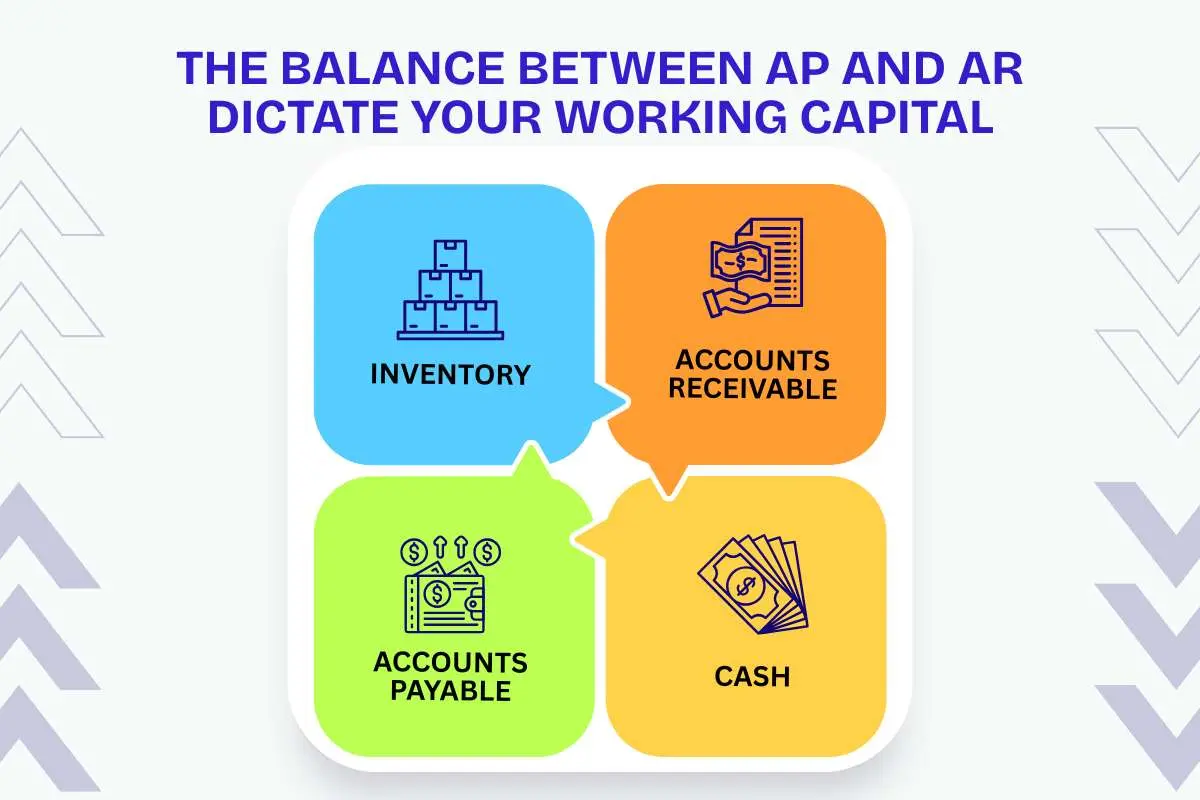

Why does the balance between AP and AR dictate your working capital?

Managing the balance between accounts payable vs accounts receivable directly impacts your corporate cash cushion. Net working capital equals your current assets minus your current liabilities. While a high accounts receivable balance increases your total working capital figures on paper, it can mask severe underlying cash flow problems.

If your customers fail to pay their invoices on time, your working capital looks incredibly healthy on your balance sheet, yet your company bank account remains empty. This friction points to the cash conversion cycle. This metric tracks the exact number of days your business takes to convert its investments in inventory into liquid cash.

Financial executives monitor these patterns via resources from the Association for Financial Professionals, which provides cash management frameworks to keep corporate spending aligned with predictable revenue patterns.

Uncovering the hidden power asymmetry

Standard accounting textbooks treat these two workflows as perfect, symmetrical mirrors. However, an operational deep dive into accounts payable vs accounts receivable reveals a hidden power dynamic that alters how you manage risk.

The core difference boils down to operational control.

The Control Profile: You possess absolute control over your accounts payable timeline. Your treasury team decides the precise afternoon to run checks, approve supplier invoices, or utilize payment terms. If you encounter a temporary cash crunch, you can choose to delay a vendor payment or negotiate an extension.

You hold zero direct control over your accounts receivable timeline. Your customer controls the payment button. Even if your invoice explicitly demands payment within 30 days, a customer might pay on day 45, day 60, or never.

This lack of control introduces credit risk and forces you to fund collection teams. If you offer 45-day terms to your buyers but your suppliers demand payment within 30 days, you build a structural 15-day funding gap. You must cover this gap with expensive bank debt or risk supply chain shutdowns.

What key metrics monitor cash flow efficiency?

To evaluate the health of accounts payable vs accounts receivable, executives track two crucial efficiency formulas: Days Payable Outstanding (DPO) and Days Sales Outstanding (DSO).

1. Days payable outstanding (DPO)

DPO calculates the average number of days your business takes to pay its bills to suppliers. A higher DPO means you hold onto your cash longer, giving you more flexibility.

2. Days sales outstanding (DSO)

DSO measures the average number of days your team takes to collect cash from customers after a credit sale. A lower DSO means you pull cash back into your business quickly.

Independent research from the American Productivity & Quality Center clarifies these performance standards. You can explore their deep-dive financial metrics directly at APQC. Their cross-industry studies highlight massive operational gaps between optimized finance departments and manual ones:

- Invoice Processing Costs: Leading finance teams leverage technology to process a single supplier invoice for $2.07 or less. Laggard organizations rely on manual data entry and spend $10.00 or more per invoice, according to performance tracking data published on CFO.com.

- Disbursement Accuracy: Top-performing organisations achieve a 98% first-time error-free disbursement rate. Manual organisations drop to an 88% accuracy rate, leading to double payments and costly billing disputes.

- Collection Velocity: Top-tier collection teams keep their cross-industry median DSO at 30 days or less. Slower organizations take 46 days or longer to secure cash from credit buyers, which locks up valuable capital.

Case study: squeezing cash flow out of a supply chain crisis

Real-world corporate performance demonstrates how compressing these cycles saves companies from bankruptcy. During a recent distribution industry shift, major suppliers began shortening their allowed credit terms from 60 days to 30 days. This change cut DPO metrics in half and forced businesses to send cash out the door twice as fast.

A mid-market manufacturing firm faced this exact problem. Their suppliers demanded cash on day 30, while their corporate customers refused to pay for 50 days. To fix this 20-day liquidity trap without relying on expensive bank lines of credit, the CFO overhauled their internal billing operations.

The company automated its collections workflow. The new system sent automated text and email alerts to customers 5 days before an invoice fell due. Additionally, the sales team introduced a 1% discount if clients settled their bills within 10 days.

This dual strategy crushed their average DSO from 50 days down to 32 days. By pulling customer cash into the bank 18 days faster, the manufacturer successfully funded their accelerated supplier obligations without borrowing a single dollar.

How does automation unify separated financial silos?

When enterprises optimize accounts payable vs accounts receivable via modern ERP automation, they eliminate manual friction. Historically, accounting teams worked in isolated rooms. The payables team handled vendor bills in one silo, while the receivables team made collection calls in another.

Integrating these workflows via modern accounting software introduces automated three-way matching. The software instantly checks the supplier invoice against your original purchase order and your warehouse receiving log. This cuts processing costs down toward the ideal $2.07 benchmark.

On the receivable side, automated cash application systems match incoming bank wires to open customer invoices instantly. This gives leadership real-time visibility into the organization’s net cash position every morning.

Frequently asked questions

1. Why should every finance manager master accounts payable vs accounts receivable metrics simultaneously?

Monitoring both metrics ensures that your cash inflows arrive fast enough to cover your mandatory cash outflows. If you look at only one side, you risk running out of cash despite showing strong profitability on your income statement.

2. What is the best way to handle a customer who lands on both the AP and AR ledgers?

When a corporate partner acts as both your supplier and your customer, accountants use a process called “netting.” You look at the balances you owe each other and execute a single payment for the net difference, which saves transaction fees.

3. Does inflation alter how a firm handles its payables and receivables?

Yes. During inflationary periods, smart companies try to increase their DPO to pay suppliers later with less valuable currency. At the same time, they lower their DSO to collect customer cash quickly before inflation degrades its purchasing power.