According to the Guinness book of world records, the most valuable life insurance policy sold was for $201 million. The advisory firm which sold the policy claimed to have negotiated with over two dozen insurers and managed complex underwriting requests from them. While limited information is freely available on social media, it might be interesting to envision the approach taken to price the risk in insurance and factors applied to underwrite the same.

Insurance companies however have been methodically pricing & underwriting the lives of customers of centuries now and data forms the DNA of a life insurer. The last few decades have seen a paradigm shift in the use of data beyond the traditional and it is interesting to write about this revolution.

Insurance is a risk management tool and insurers require a robust framework to be able to run a business which buys risk & manages the same. Risk classification is usually customized to the industry & in most instances for each organisation. A simple approach to risk management entails identification of risks both top down & bottom up, measurement of impact & likelihood, reporting to key stakeholders, development of a mitigation plan, tracking the same & managing residual risk.

Anything which has an impact on the vision & mission of a business and hence affects the delivery of its goals is a risk. Risk would be embedded at each stage of the customer life cycle & the insurance policy lifecycle. It’s sometimes easy to identify and comment on an aspect of the business function and cite risks. We can manage the risk & benefit from it only if it is sized and analysed if it fits within the organisation’s appetite. It’s a double- edged sword.

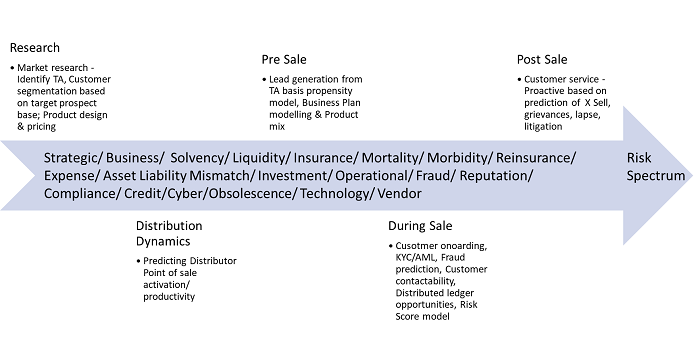

If we do not leverage risk, we may not only miss out on an opportunity but get consumed by the underlying threat. We have outlined the relevance of data and analytics at six stages of the business and how it has an impact on the spectrum of risks the organisation is faced with.

Research:

The actuarial and product would be able to develop & price a product only if they have a good understanding of the customer need by segment. In an era of hyper localization, development of customer personas which are aligned to the business vision and creation of bespoke propositions for each involves a razor-sharp use of market research and leveraging appropriate distribution. As this a nascent industry in the country, products are regulated to ensure that the customers interests are kept at the centre.

This calls for a tight rope walk. If the pricing goes astray or if the customer segmentation & product proposition are not basis the persona, the company is exposed to strategic risks. After getting all this right, if the distribution is not aligned, we run a business risk.

Distribution Dynamics:

Insurance is a distribution-oriented business, be it online, bancassurance, agency, broking, or micro channels. Acquiring new distribution in a crowded market is tough and farming existing distribution to its optimum potential and smart use of data can play a key role in the same. The success of digital channels is entirely dependent on the smart use of data. Activation & productivity are the key vectors to work with any distributor and predicting the impact on input factors of product, pricing, training & motivation on the same can be done using propensity models.

If a newly acquired distributor is not leveraged, the company runs the risk of losing them soon. Similarly, innovating number crunch can lead to recruitment of the right person for the right role and commence the road to success for the employee leading to lower attrition & higher productivity.

Pre-Sale:

In addition to developing scenario based plans & planning for a product mix which helps the business meet its customer needs whilst achieving the organisational goals, lead management is a big area where the right use of data can help leverage the tools available. Propensity to buy models can be implemented at a customer level to help the sales channel to pitch a need-based solution and is likely to increase the lead to conversion success ratio. A delighted customer & hence a happy distributor augur well for the business.

During Sale:

Life insurance and annuity contracts are for the long term laced with a low magnitude of transactions during the tenure. Onboarding a customer with the help of smart tools to do available today eases his transaction and help prevent fraud. In addition, they help strengthen underwriting if the risk score triggers additional controls. Organisations like Insurance Information Bureau promoted by the Indian regulator IRDAI fill the need for sector level data repository and analytics. Operational, Insurance & Regulatory risks are overcome by smart use of data at the time of sale.

Post-Sale:

Engaging a customer is key to retaining the customer to maturity. Customer satisfaction indices like CSAT, NPS & persistency serve as a barometer and guide customer engagement to nurture the promoters, motivate the passives, and win over the detractors. This helps overcome risks of lapsation & litigation. If leveraged well, this can result into upsell opportunities.

In addition to the above where smart use of data is featured across functions & customer lifecycle, we have seen innovative usage across the supply chain and all stakeholders. Healthy returns from the investments made by an insurance company are essential for delivering the assured returns in guaranteed offerings and garnering customer delight by beating market benchmarks in unit linked offerings. This is another function which harnesses data to manage customer aspirations.

About The Author- Sunder Natrajan, Chief Compliance & Risk Officer, IndiaFirst Life Insurance Company Limited

Sunder Natarajan is the Chief Compliance & Risk Officer and oversees the risk, compliance, internal audit and legal functions at IndiaFirst Life. He is responsible for embedding the risk management framework along with the implementation of good corporate governance in the organisation.

His noteworthy achievements at IndiaFirst Life include spearheading the bancassurance distribution strategy for the company and helping build an integrated bancassurance model with partner banks. Additionally, he set up the sales training team and launched mobile learning for the sales and distribution partners.

Sunder’s work experience in the insurance industry spans for two decades with proven excellence across diverse functions including Sales, Customer Service, Strategy, Bancassurance, Customer Retention, Operations, Quality, Business planning, Training, Communication & Governance. He has also held stints at companies like Aviva Life, Royal Sundaram General Insurance & Ogilvy Public Relations Worldwide.

He is on the strategic advisory board of the Institute of Risk Management India Affiliate and is the Deputy Chair for the IRM India Regional Group.

Sunder holds a Bachelor of Commerce degree from the University of Madras and Post Graduate Diploma in Business Administration from NMIMS, Mumbai. He completed an Accelerated Leadership Program from Indian Institute of Management, Ahmedabad and is a Certified Member of the Institute of Risk Management, London.